Distributors have a harder time building business and profits if they don’t understand their cost-to-serve (CTS) and apply it to pricing decisions. The marketplace has changed drastically, and the standard cost-plus margin approach is unlikely to cover their bases across the board. Competition has crowded in, driving down gross margins and increasing customers’ expectations for service. Cost-plus pricing doesn’t account for these changes, and it doesn’t factor in how demands and behaviors vary among customers.

If you’re in the industry, you want to raise the bar at your organization, providing added services to maintain customers and compete. But you don’t want to lose money on individual sales in the process. To ensure your efforts will be profitable, assess your CTS. A clear view of CTS in your customer mix will help you determine the correct route to growth and optimal profitability.

Best Practices for Calculating Cost-to-Serve

Calculating and using cost-to-serve can be complex. The more complicated it is to use and apply to customers, the more difficult it will be to get buy-in from your sales force. Additionally, a more complex approach means more time and effort. For these reasons, distributors tend to neglect CTS altogether and instead opt for cost-plus pricing.

Some distributors try a one-factor approach to CTS. They’ll use one component, such as sales or transportation cost, to measure CTS. This is a good practice, but it’s not the best.

There are two best practices we’ve discovered in our research and through our experience in the industry:

Activity-Based Costing (ABC)

Activity-Based Costing is a widespread best practice for calculating CTS. However, ABC is complex and work-intensive, and calculating it takes a significant investment in time and resources. It tends to fall flat when it comes to adoption by sales reps and other key personnel, though there are distributors that have been successful applying ABC in their pricing decisions and in dealing with customer relationships. This practice involves using formulas to allocate certain expenses (e.g., warehouse expenses, shipping expenses) to individual orders to arrive at a more exact CTS for each customer. Adding this to the gross margin to find the net profit (NP) can help you rank your customers. Because it is so work-intensive and takes so much time, sales forces may not accept it, as occurred with one distributor that used ABC to determine per-unit loading costs. The calculations showed that the cost in Corpus Christi, Texas, was 50 cents per pallet and the cost in Denver, Colorado, was $5 per pallet. Their sales force rejected this analysis as untrue.

Surrogate Method

The Surrogate Method is a simpler, easier-to-use model for calculating CTS. With it, you use activity-based methods along with other criteria like average order size and returns. And instead of ranking customers based on a more exact CTS, you’re ranking them as they compare to one another. It’s as effective as the ABC approach, but it tends to get markedly greater buy-in and ROI. The simplicity of the method makes it easier for salespeople to adopt and explain it to customers. It also makes for faster implementation, and distributors already have the data they need to conduct these calculations and rankings in their systems.

Critical Factors for Calculating CTS

The factors that are relevant to calculating and using CTS typically fall under finance, operations and sales. In our research, we’ve found 21 potential factors distributors can use to understand CTS. But not all of them are effective when you’re ranking customers by comparison. To identify the best factors at your organization and among your customer mix, each factor should meet the following criteria:

- Has measurable data associated with it.

- Can be quantified at the customer level.

- Is applicable for every customer.

- Can be understood by each sales and pricing influencer.

The factors that meet these criteria are the ones you can use to determine CTS and segment your customers. We’ve found seven critical factors that apply across customers at most wholesaler-distributor organizations:

- Average Order Size ($): Order sizes affect CTS from both a handling and delivery-cost standpoint. Frequent small orders create higher handling costs than less frequent, larger orders.

- Average Number of Line Items: Small orders with few line items can drive your CTS up, particularly if a customer repeatedly places a large number of small orders. Single-item orders have their associated expenses, like picking, trucking and delivery. You get a lower CTS and more efficient business with more line items per order.

- Days to Pay: Days to pay is one of the most significant CTS factors, so distributors benefit from careful monitoring and improvement in this area. The more days to pay a customer takes on an order, the greater the opportunity cost (of capital). Minimizing days to pay can drastically improve the cash conversion cycle, resulting in better cash flow. In terms of accounts receivable, the risk increases the longer it takes for customers to pay for their orders.

- Will-Call Orders (%): It’s common for customers to pick products up from distributor facilities or warehouses as opposed to having them delivered, especially in specific trades, such as industrial and HVAC/plumbing. These will-call orders affect CTS, reducing transportation and delivery expenses. This translates to fewer resource commitments for these customers, lowering their CTS considerably.

- Same-Day Deliveries: Same-day deliveries often result in greater transportation and inventory costs than other delivery options, such as next-day. When customers request more same-day deliveries, distributors may not have enough lead time to plan and fulfill orders efficiently. It’s convenient for customers to get products immediately, but if same-day deliveries become a constant, it could indicate poor inventory planning on the customer’s part. Same-day delivery is a critical CTS factor because it directly impacts the cost to serve customers in multiple categories, including finance, sales, and operations. For more deliveries, distributors need more inside sales resources, incur greater transportation, inventory and order processing expenses, and require more time-to-plan logistics (scheduling, routing and cubing).

- C and D Items Accessed: Customers who order a product mix that contains a high portion of C and D items, which typically move slower, tend to have a higher CTS than those customers whose product mix includes a high proportion of A and B items, which are fast-moving.

- Number of Returns: Customers who regularly return items from orders have higher handling costs and possibly stock-out costs. Each return order comes with a slew of paperwork and requires resources in the supply chain because it involves suppliers. Managing and monitoring this factor requires more discipline from a data-entry perspective. For each product return, the distributor must capture the reason. If the cause is not captured accurately, customer stratification and analytics could penalize customers for the wrong reasons.

Putting CTS into Practice

A regional distributor that was growing via acquisition had 22 stocking locations while selling across two states. The distributor’s CTS was high, and it didn’t have a consistent pricing mechanism for all locations. The leadership team wanted to deploy a pricing framework across all locations that their sales force would readily adopt. However, they didn’t have education and training around CTS, which was pivotal for positioning the sales force to embrace and adopt the new pricing recommendations. To ensure adoption, the leadership team needed to help the sales force understand CTS and how it affects pricing.

First, they gathered stakeholders from across departments, including sales, operations, finance and purchasing, to determine which CTS factors were most pertinent. The CFO preferred a comprehensive set of 11 metrics, but the VP of Sales preferred a simpler approach with only the most powerful metrics. A simpler approach was more likely to gain buy-in. Together, they selected: Average order size, number of line items and days late.

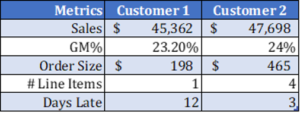

Having these CTS factors selected made it easier to get sales and other customer-facing roles on the same page. In the table below, we compare two customers with similarities side-by-side. Their sales and gross margin are alike, and it doesn’t appear that pricing needs adjusting for either. But when you factor for CTS, it’s clear that pricing adjustments should be made to minimize CTS.

The customers’ margin percentages are similar even though it’s clear that Customer 1 places more than twice the number of orders as Customer 2. Customer 1 is ordering a single item per order and paying late by 12 days on average. Customer 1 costs more to serve and has a similar margin to Customer 2. Seeing this, the sales team can see the reasoning for the new pricing mechanism and accept it. They simply needed a framework for and training around CTS.

Pradip Krishnadevarajan is co-founder of ActVantage, which helps distributors drive profitable growth through analytics. He has more than 15 years of experience helping hundreds of distributors while co-authoring seven books for the National Association of Wholesaler-Distributors. He recently released a margin recovery guide for distributors to use as they manage through the coronavirus pandemic. Before joining ActVantage, he co-founded the wholesale distribution-focused research lab at Texas A&M University’s Industrial Distribution Program. Contact Krishnadevarajan at pradip@actvantage.com or visit actvantage.com.

Related Posts

-

Building materials distributor SRS said it has named Ryan Nelson to the company’s top financial…

-

Greenfield locations will play a key role in SRS Distribution’s expansion plans in 2021.

-

RB operates two marine distribution and fabrication facilities, located in New Orleans and San Diego.