The Institute for Supply Management released its monthly manufacturing Purchasing Managers Index (PMI) on July 1, reflecting June activity, which revealed a moderate month-to-month improvement in U.S. industrial activity.

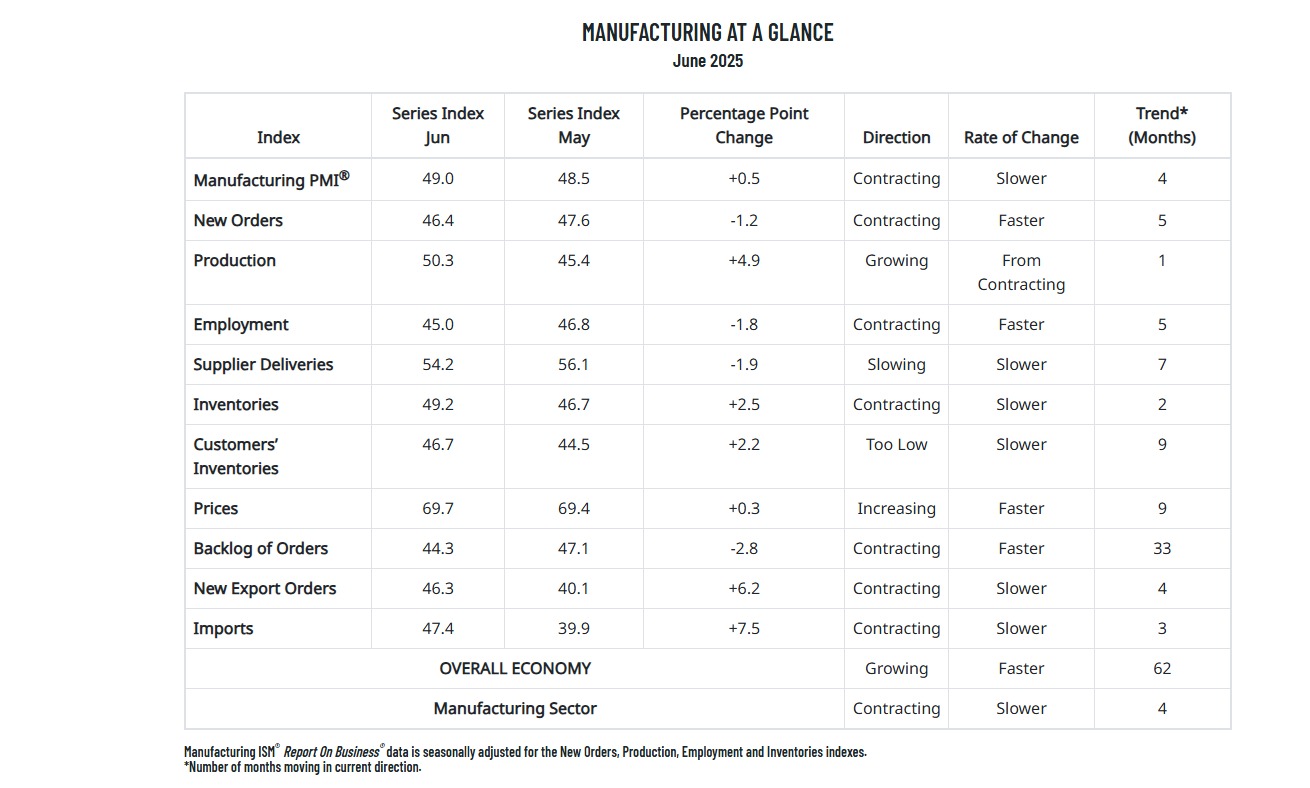

The PMI — regarded as a key indicator of U.S. industrial health — was up 0.5 percentage points month-over-month to a reading of 49%, following a 0.2-point drop during May. It marked the fourth straight month that the PMI was in contraction territory (anything below 50.0%) after a brief expansion in January-February preceded by 26 months of contraction.

The June increase was above expectations of a rise to 48.8% forecasted by economists polled by major news outlets.

More granularly, the latest report showed that output revealed mixed results in June, with the PMI’s subindex for production up 4.9 points to 50.3%, while new exports likewise increased 6.2 points, but remained in contraction territory at 46.3%. Reflecting demand and tariff pricing, the imports index remained in contraction territory in June but increased 7.5 points to 47.4% after plummeting to 39.9% in May. Meanwhile, the index for new orders contracted for a fifth month in a row, declining 1.2 points to 46.4% but prices increased 0.3 points to 69.7%.

In the Store: MDM’s U.S. MRO Market Trends Report

Of the five subindexes that directly factor into the PMI, two — production and supplier deliveries — were in expansion territory, up from one in May.

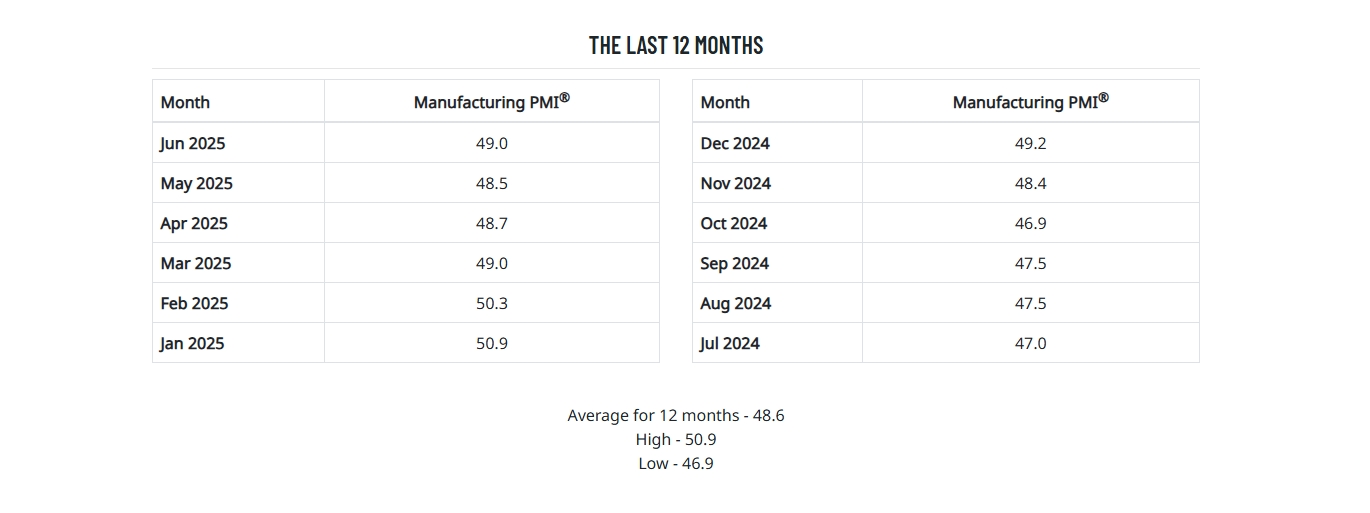

Here’s how the overall Manufacturing PMI has looked in bar chart form over the past 12 months:

source: tradingeconomics.com

Of the 17 manufacturing industries the PMI reflects, nine reported growth in June, led by Apparel, Leather & Allied Products and Petroleum & Coal Products. The six industries reporting contraction were led by Textile Mills and Wood Products.

MDM Case Study: MSC Industrial Supply (Premium access here)

PMI Respondent Commentary

- “Business has notably slowed in last four to six weeks. Customers do not want to make commitments in the wake of massive tariff uncertainty.” [Fabricated Metal Products]

- “Middle East unrest as well as unstable long-term tariff positions continue to impact second- and third-tier sources, which is applying pressure to material costs. Costs are up 6 percent to 10 percent over budgeted inflation — and the forecast accounted for the volatility expected with the current administration.” [Wood Products]

- “The biopharmaceutical space is starting to see more pronounced headwinds: Stock prices have significantly eroded, companies are facing hiring freezes, and so on.” [Chemical Products]

- “The tariff mess has utterly stopped sales globally and domestically. Everyone is on pause. Orders have collapsed.” [Machinery]

- “Tariff volatility has impacted machinery, steel and specialized components. Also, potential shortages of skilled labor for construction, maintenance and installation.” [Food, Beverage & Tobacco Products]

- “Tariffs continue to cause confusion and uncertainty for long-term procurement decisions. The situation remains too volatile to firmly put such plans into place.” [Computer & Electronic Products]

- “Tariffs continue to impact material pricing.” [Petroleum & Coal Products]

- “Tariffs, chaos, sluggish economy, rising prices, Ukraine, Iran, geopolitical unrest around the world — all make for a landscape that is hellacious, and fatigue is setting in due to dealing with these issues across the spectrum. Unfortunately, this is just the beginning unless something drastically changes, but the supply chain implications will grow — depots will not be stocked, less material will be available, and it will take years for domestic production to handle the needs (if companies even want to).” [Primary Metals]

- “The geopolitical environment remains volatile: (1) ongoing shifts in U.S. tariff policy make it difficult to plan, (2) emerging conflicts in the Middle East could pose long-term commodity risks and (3) China measures on rare earth materials are causing challenges. Overall outlook for our company is positive; it’s just extremely hard to make near-term supply plans/strategies or budgets.” [Miscellaneous Manufacturing]

- “The word that best describes the current market outlook is ‘uncertainty.’ The erratic trade policy with on-again/off-again tariffs has led to price uncertainty for customers, who appear to be prepared to hold off large capital purchases until stability returns. This has resulted in further reductions in customer demand and softening sales for the balance of 2025. Operations has planned additional weeks of downtime at multiple plants to accommodate reduced orders. Next year’s forecast is not any better at this point. Additionally, most electric vehicle (EV) projects have been delayed or canceled, resulting in a significant amount of unutilized capital investment. EV technology launches for 2026-28 have been delayed past 2030.” [Transportation Equipment]

Related Posts

-

A new chair will succeed Timothy Fiore in June 2025 to lead ISM’s Manufacturing Business…

-

Following two consecutive months in expansion territory, March fell back into contraction and below economists'…

-

The December PMI report showed a rebound in production and a rise in new orders,…