Editor’s Note: This is the first article in a three-part Premium series that analyzes MSC Industrial Supply and its company evolution. Stay tuned for Parts 2 and 3, as well as a comprehensive MDM Case Study report that packages this series with additional insights.

This MDM Case Study article series on MSC Industrial Supply (MSC) was exciting to work on, as it is a leading distributor making public and major model adjustments in the B2B supply channel. The company’s journey from a “catalog” spot-buy distributor to what MSC calls a “mission critical” distributor has been fascinating to observe. Of all the public distributors we’ve written about extensively in this series (Ferguson, Wesco, Watsco, Fastenal, etc.), MSC has made the largest number of public strategic and tactical adjustments to its successful model over the past 18-24 months.

How MSC Got Here

Melville, NY and Davidson, NC-based MSC was founded in 1941 as Sid Tools in New York by Sidney Jacobson, who sold cutting tools and accessories to machine shops. That initial focus on the machine shop has been the core foundation of MSC’s growth to a $3.8 billion revenue company in its 2024 fiscal year (Sept.-Aug.). The focus on the metalworking spindle has been the core business foundation that drove the company’s growth from a single store to a national distributor. The other key driver was MSC’s wise, early investment in data and technology. MSC was one of the first distributors in North America to invest in computerized inventory management and order processing.

Using the Big Book was how you ordered. Search for the item you want, find the page and the part number and then call or email your MSC inside sales representative (or order directly online starting around 2000). Where MSC differed slightly from Grainger’s “Red Book” was the breadth of offerings; MSC focused on metalworking while Grainger was more broadly general industrial and MRO.

MSC was a catalog house specialized in serving metalworking end customers who depended on it to get products the next day to run their business. Until the 2000s, the MSC/ Grainger/Fastenal-type industrial catalogs were the human search engines for the business.

These catalogs were the easy button of ordering for end customers. To use a grocery store analogy, the Big Book was the aisle that customers traversed with their shopping cart and the catalog occupied shelf space, giving them repeat business at strong margins.

One of the key differences between MSC and distributors like Grainger and Fastenal was MSC was not historically a branch-based distributor with thousands of local branches to serve end customers. That distinction is important as we dive into this MSC series.

So, let’s start with the biggest strategy adjustment for MSC in the past year or so: a pricing reset.

Pricing Reset: The Most High-Risk, High-Reward Activity in Distribution

As a former pricing leader for three different billion-dollar distributors in North America, I can share that a major pricing reset is simultaneously a dangerous activity, yet when done right, the best driver of top-line sales growth in this industry.

In March 2024, MSC Chief Financial Officer Kristen Actis-Grande announced during a Raymond James investors conference that the company was in the process of “fixing” the list price structure the distributor has “used for the past 20 years.”

Why is MSC making this major change and why is it crucial to their growth plans? As Actis-Grande shared, “for non-contract customers, our list price — the price they viewed — was considered not fair and credible.”

To add context to that comment, when a non-contract customer would go to mscdirect.com to order one of the company’s 2.4 million SKUs, they would likely see what I’d call an unrealistic price. Over time, more of these customers leave the MSC web platform and find and order these SKUs somewhere else.

MSC’s On Account customers (customers with an account number) have an online login that ties to their account. So, when an MSC On Account customer searches for products online, they see their expected price.

MSC’s eCommerce business represents 63.7% of the company’s total business in its fiscal 1Q 2025 (spanning Sept.-Nov. 2024), according to earnings reported on Jan. 7, 2025. This percentage underscores why having the right MSC online price is so important to the business.

You may be reading this and thinking it’s not a big deal. Non-account customers are smaller accounts and cherry-pickers, so it’s not a material impact on the business. There is some validity to that statement, but over time, that loss in customers is like a melting ice block and does curtail top-line sales growth. So, let’s dive deep into why MSC’s lack of a credible online price for non-account customers needed to be adjusted.

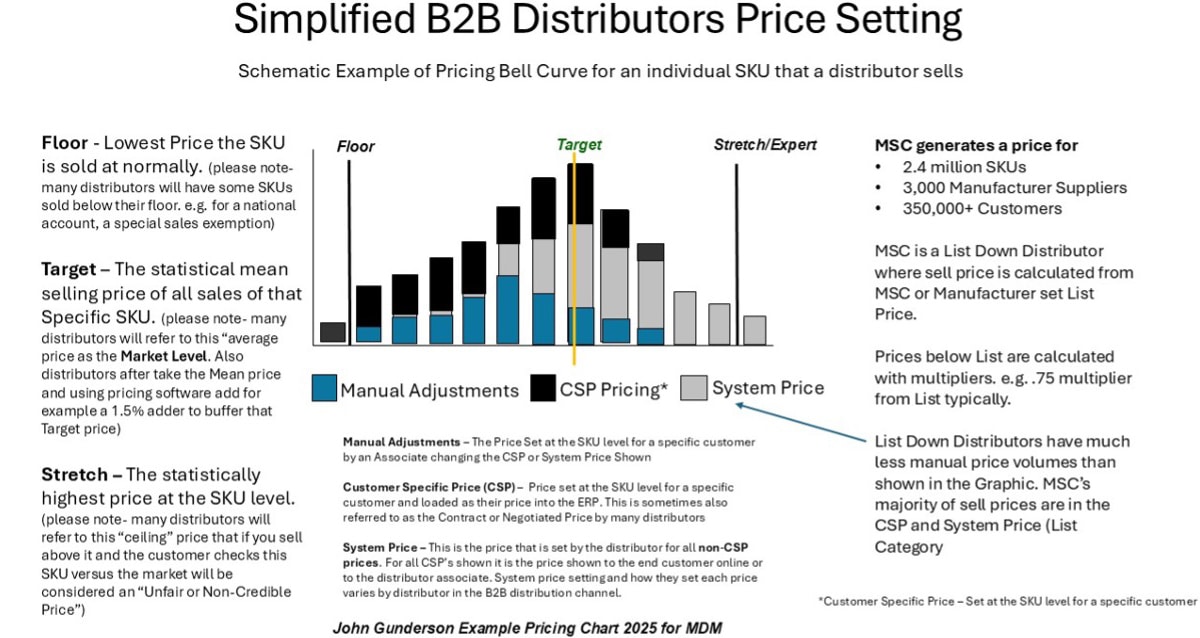

The schematic example above is a high-level illustration of how the sell price is calculated/analyzed at most B2B distributors. Most pricing engines from service providers have a similar approach (floor/target/stretch).

At the SKU level, all sell prices are analyzed from lowest to highest (for a 6 to 12-month period, typically) and the statistical mean for that SKU sale is roughly the target level. There are many other factors — including size and type of customer and order type (stock versus direct) — used in floor/target/stretch pricing, but to keep the example simple, I have not shown that complexity.

Many distributors consider the target price as the “not to sell below price.” It is considered the market level or “a fair and credible price” for their customers.

The floor also can be set during this process at the SKU level and this is considered the lowest level you should sell a product at, but, when you do, it has to have management sign-off and be for a strategic reason — e.g. for a top customer, “if I sell this SKU I get these other higher margin sales,” etc.

The stretch/expert level is the highest price the math shows the market will bear. I often referred to this as the ceiling. The danger of the ceiling is if you have too much of your sales for a customer close to the ceiling, they often will reduce volume, as they do not see what they perceive as a fair and credible price.

Setting sell prices for every distributor is very difficult and an ever-changing target. The challenge for MSC is it must set prices for 2.4 million SKUs for hundreds of thousands of customers and 3,000 suppliers. In my opinion, the complexity and nuance of that work is three to five times more than, say, an electrical, HVACR or construction supplies distributor faces. MSC has many more total SKUs to price than the distributors in construction supply and more focused industrial channels.

MSC is focused on manufacturing and machine shops as the majority of its revenue stream. At the Raymond James conference in early 2024, Actis-Grande noted that metalworking represented 45% of total business.

MSC is not what I would call a branch-based distributor, as it has 40 North American locations (including five Central Distribution Centers) compared to Fastenal’s ~1,600 and Grainger’s ~300. In comparison, MSC does not have a large counter business (customers who come to a location to pick up orders).

Because of this dynamic, industrial MRO distributors and their culture typically don’t allow associates to “override” the suggested sell price at the same levels. Overrides are considered by many B2B distributors as “margin erosion” or having a sales team that cannot “sell their value.”

I don’t believe that override elimination is a black-or-white issue, because if the sell price you present to the customer is not viewed as “fair and credible,” you will lose sales volume long-term.

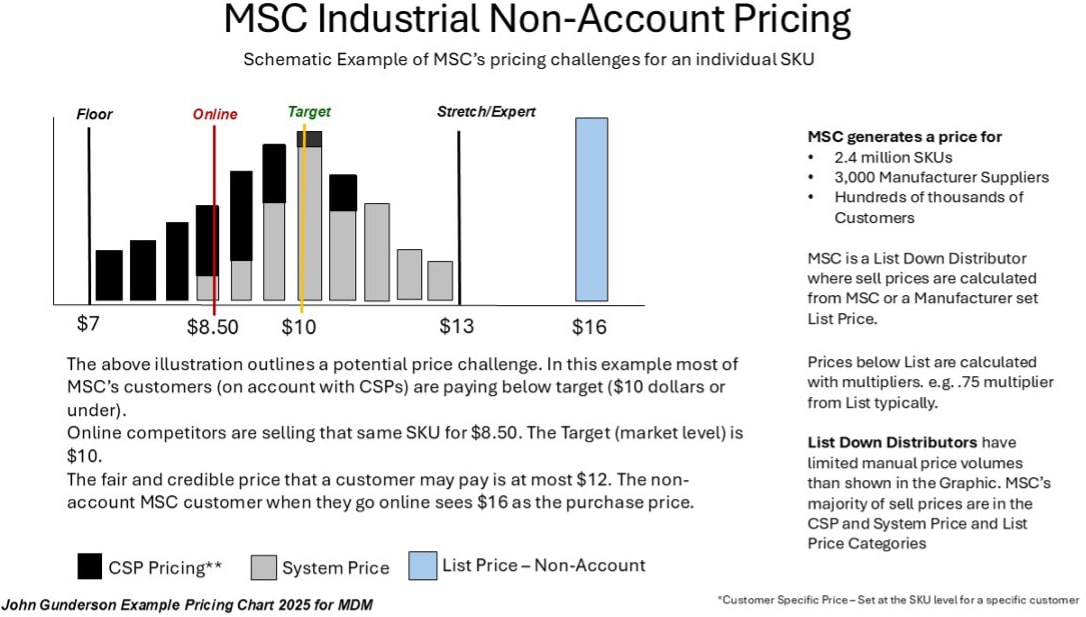

As you examine the above graphic, it is important to understand the dynamics MSC faces that drove the decision to reset pricing for non-account customers.

Overrides or manual pricing are generally not a lever MSC uses as often as other distributors. (Note: MSC associates are likely highly involved in setting pricing for On Account Customers for CSP pricing).

In the example above, I created a fictitious SKU that, when we did the math, showed a suggested target price of $10 as a sell price. The floor was calculated at $7 and the stretch/ceiling at $13. So, let’s say this is a high-volume selling SKU that has many other online competitors selling this same product. The target “market level” price for MSC is $10 and the competition, to earn business online, ends up monitoring that price and decides to price below that at $8.50.

The list price that an MSC non-account customer sees is $16. If visitors think that it seems high and search, they will find that they can buy it for almost half price elsewhere. The long-term outcome on volume reduction and smaller customers is obvious.

I can share that I have been in MSC’s shoes, so to speak, where the non-account business margin (List Price) is significantly higher than your CSP margins. The list price you have that customers pay significantly adds percentage points to your overall margin profile.

So, often your distribution business is very reluctant to reduce its dependence on the List Price – also known as third column price. As a distribution pricing leader, many times you are measured only on the overall margin percentage. When gross margin percentage (GM%) goes down or up, you get blame or credit. So, you and your pricing team may view this list business as untouchable. Conversely, the sales leaders get all the credit and the blame for everything good and bad that happens with sales.

Organizationally, that list price/third column GM% can be organizationally like a block of ice that is highly valued. The challenge today is the size of that block of ice is slowly melting away because the market conditions have changed over the past 20 years. The intensity of the sun is increasing every year (online competitors mean customers have more choices to buy similar products elsewhere).

MSC has undertaken an effort to fix that issue over the last year, and there’s no easy button for it. A major pricing reset is an in-the-trenches, challenging work process. It has not been easy for MSC on their pricing reset journey and they publicly have shared those difficulties, but it has been resolute in this effort and shared recent improved progress.

Another Recent Reset Example

MSC has a unique position as a distributor, but it has a peer distributor that has undertaken a similar List Price project in Grainger, which sits atop MDM’s Top Distributor lists for industrial supplies and MRO and appears on numerous others. MDM extensively covered the company’s pricing reset that it started in 2017.

In the long term, Grainger was very successful with its pricing reset. Some would say it “bit the bullet” and did what it had to face online competition like Amazon and others.

I predict that MSC’s effort to create “fair and credible prices” may also, in the long term, help the company’s coordination between sales and operations (pricing/purchasing/logistics). In my opinion, MSC is now conducting a pricing reset that is highly likely to be successful because it will likely drive more internal collaboration.

The Big Takeaway

So, what can you learn from the moves the MSC is undertaking as a channel leader?

My advice is that, if you have a significant list price/third column business, dive into the data, look in the mirror and ask yourself, “Can we look at this differently? Are we losing customers or reducing their sales volume because we are priced out of the market?”

Conversely, if you as distributor or manufacturer are generally giving all the sales credit/blame to the sales team and all the margin credit/blame to the pricing/inventory teams and incenting your teams accordingly … try to change that. Sales need fair and credible pricing and your business needs margin percentage and dollars to perform.

The best distributors and manufacturers know that sales and margins are connected and not the exclusive domain of either sales or pricing/operations.

Up Next

In part 2 of our series, we will dive deeper into MSC’s strategic initiatives and growth plans and its continued progress in evolving as a “mission critical” distributor.

MDM’s Case Study Series

- Watsco (in Premium Dashboard here, in MDM Store here)

- Ferguson (in Premium Dashboard here, in MDM Store here)

- Wesco International (in Premium Dashboard here, in MDM Store here)

- Fastenal (in Premium Dashboard here, in MDM Store here)