The U.S. economy had stronger-than-expected growth during the third quarter, according to a long-delayed report from the Commerce Department.

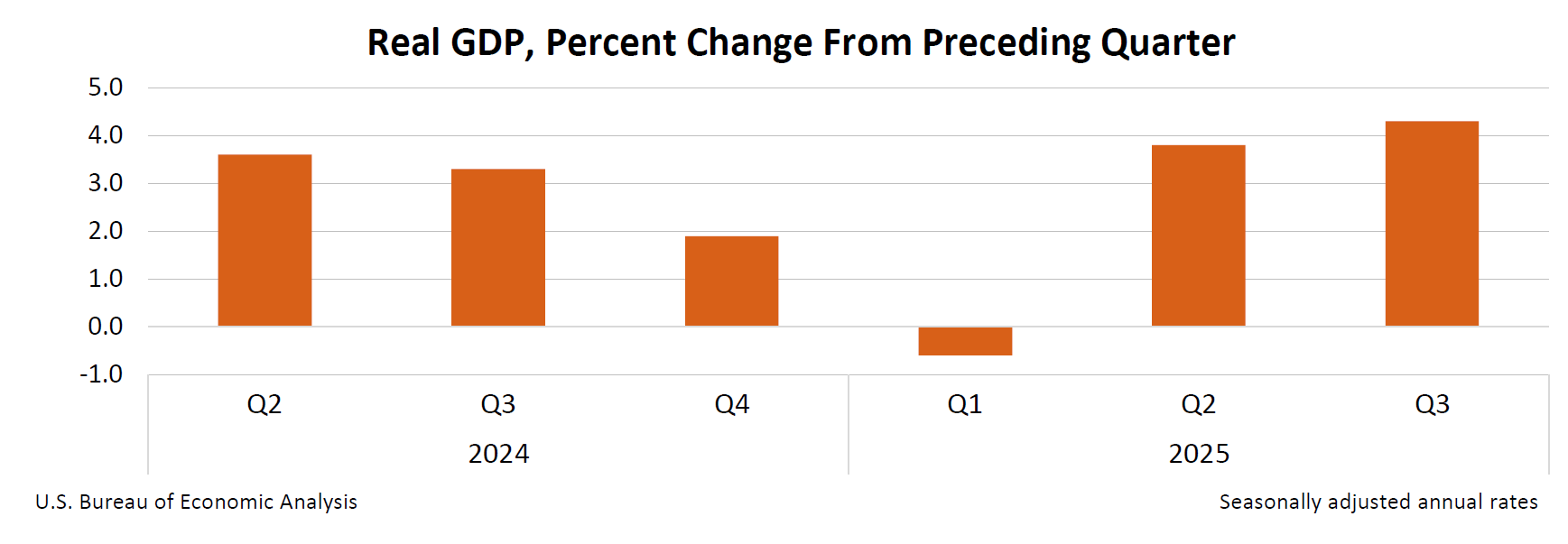

Postponed by the government shutdown that spanned Oct. 1-Nov. 13, the advance estimate report said the economy expanded at a 4.3% annual rate in the July-September period — marking the strongest growth rate in two years — powered by strong consumer spending.

That accelerated from Q3’s 3.8% growth was far ahead of the 3.2% forecast from economists polled by the Wall Street Journal.

The Bureau noted that the Dec. 23 report replaces the release of the advance estimate originally scheduled for Oct. 30 and the second estimate that was set for Nov. 26.

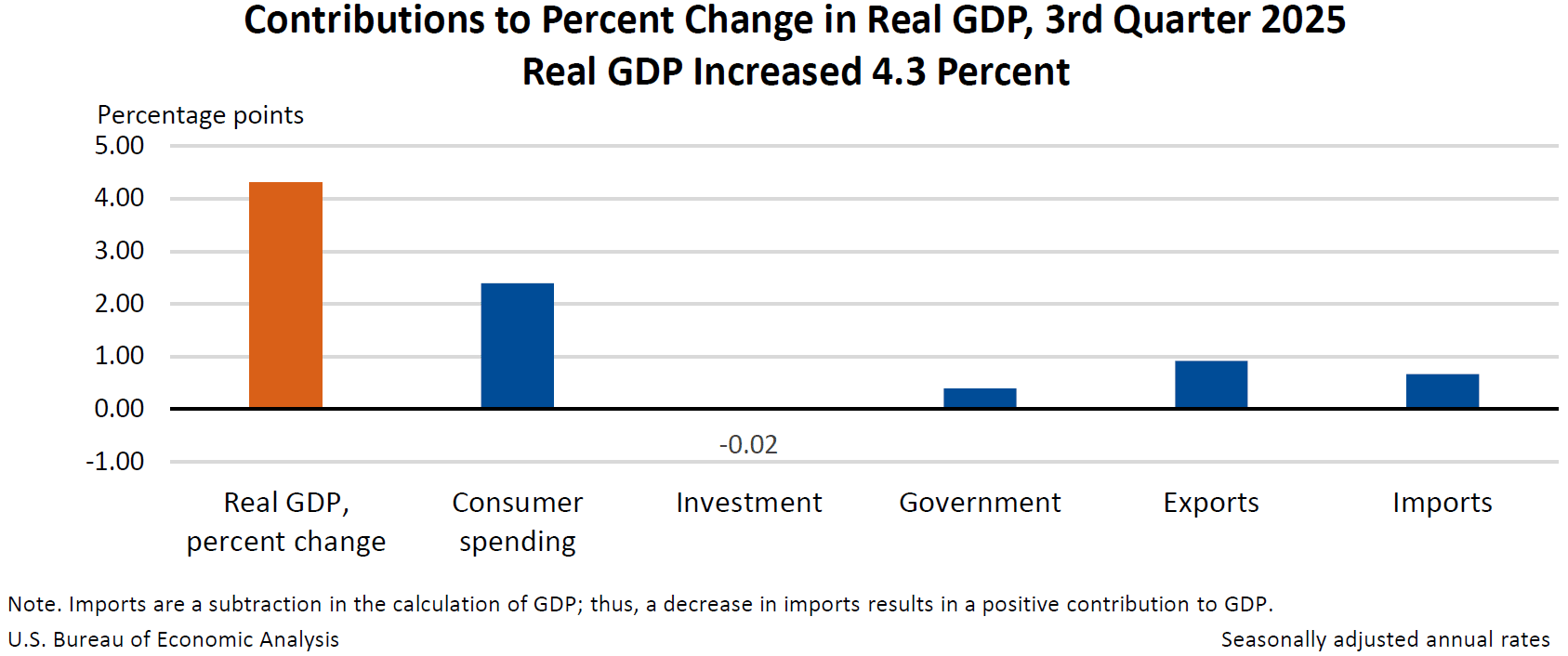

The Bureau noted that the 3Q growth increase primarily reflected an increase in consumer spending — particularly in recreational goods and vehicles, prescription drugs and health care and other services — alongside upturns in exports and government spending. Meanwhile, imports decelerated.

Consumer spending grew at a rate of 3.5% in 3Q, rising from 2Q’s 2.5%, and investment in equipment and intellectual property — which includes AI-related spending — rose 5.4%. Within nonresidential investment, equipment investment rose 5.4% while structures fell 6.3%.

Trade had a net 1.59 percentage points impact on top-line GDP, with exports jumping 8.8% while imports fell 4.7%.

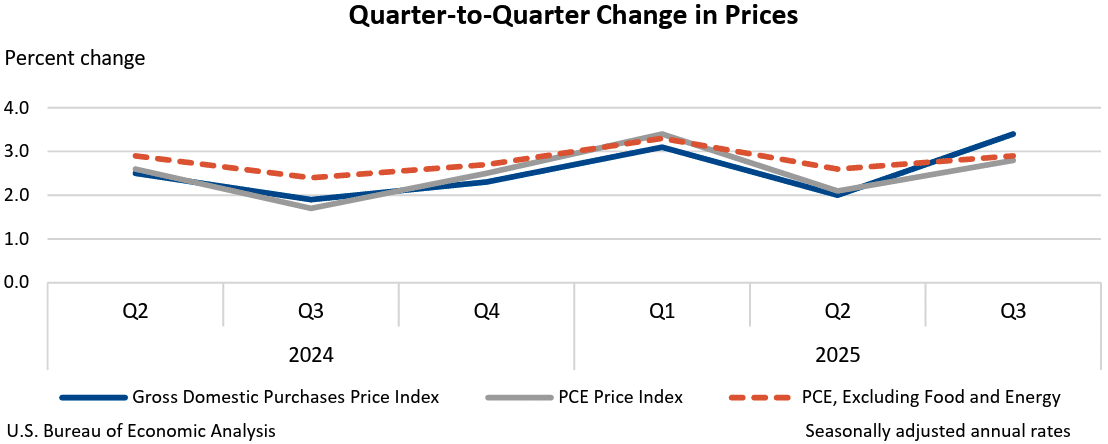

On the pricing front, the price index for gross domestic purchases increased 3.4% during 3Q, accelerating from 2.0% in 2Q, while the personal consumption expenditures price index (PCE) likewise moved up 70 basis points to 2.8%. Excluding volatile food and energy prices, the PCE price index increased 2.9% in 3Q, up from 2.6% in 2Q.

MDM Analysis

As we noted about the Bureau’s third estimate for 2Q GDP, tariff impacts still cloud the country’s true economic growth. Inflation picked up in 3Q alongside consumer-driven economic growth, with core PCE prices accelerating at a rate well above the Federal Reserve’s 2% target. The Dec. 23 report is the government’s first official estimate for 3Q growth, and it arrives as fourth quarter is about to close. The Commerce Department and all other government data agencies are still in catch-up mode and will be through at least January. Meanwhile, U.S. unemployment rose in November to its highest mark in over 4 years at 4.6%., and contractor-heavy retailers like The Home Depot cut their full-year outlook, citing consumer hesitation.

As usual per lately, it’s an overall mixed bag of economic signals, though the top line GDP figures can’t be ignored as an indicator of broader growing strength — at least entering October.

2Q imports plummeted 29.8% during 2Q after surging 37.9% in 1Q as wholesalers and manufacturers rushed to front-load inventory before widespread tariffs went into effect at the start of April. Imports contributed 5.09 points (revised up from 4.99) to the updated GDP figure after negatively impacting it by 4.66 points in 1Q. Consumer spending — the largest driver of the U.S. economy — improved in 2Q with a 1.07-point contribution (revised up from 0.99) after just a 0.31 impact in 1Q.

| Real GDP and Related Measures (Percent change from 2Q to 3Q) |

||

|---|---|---|

| 2Q 3rd Estimate | 1Q 1st Estimate | |

| Real GDP | 3.0 | 4.3 |

| Current-dollar GDP | 5.0 | 8.2 |

| Real final sales to private domestic purchasers | 1.2 | 3.0 |

| Real GDI | … | 2.4 |

| Average of real GDP and real GDI | … | 3.4 |

| Gross domestic purchases price index | 1.9 | 3.4 |

| PCE price index | 2.1 | 2.8 |

| PCE price index excluding food and energy | 2.5 | 2.9 |