The U.S. Census Bureau released its monthly construction spending report on July 1, covering data for May 2026.

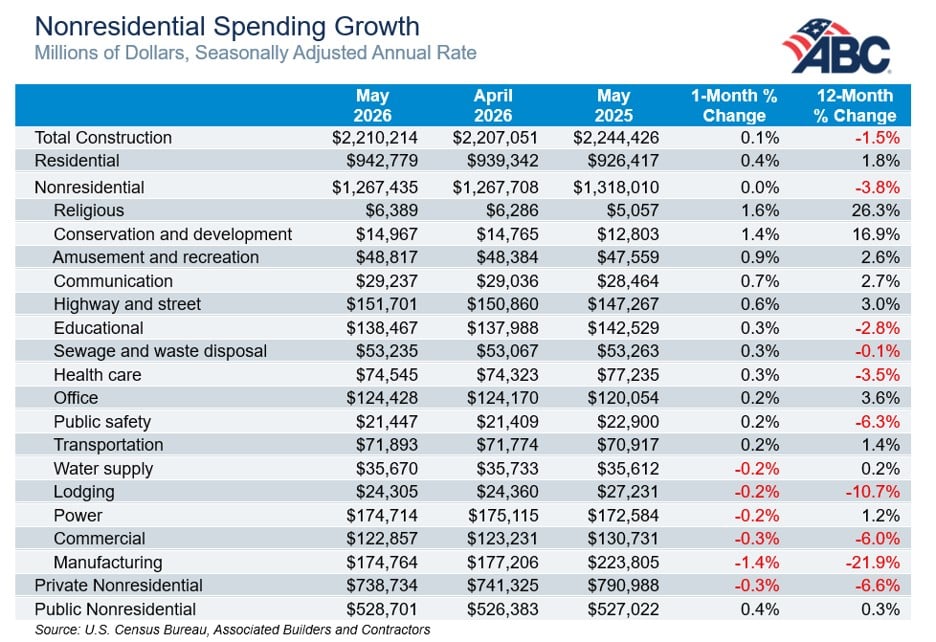

The Bureau’s report shared that May total construction spending was estimated at an adjusted annual rate of $2.210 trillion, up 0.1% from April’s revised mark, but down 1.5% year-over-year. During the first five months of 2026, construction spending totaled $858.4 billion, down 2.7% from the same period in 2025.

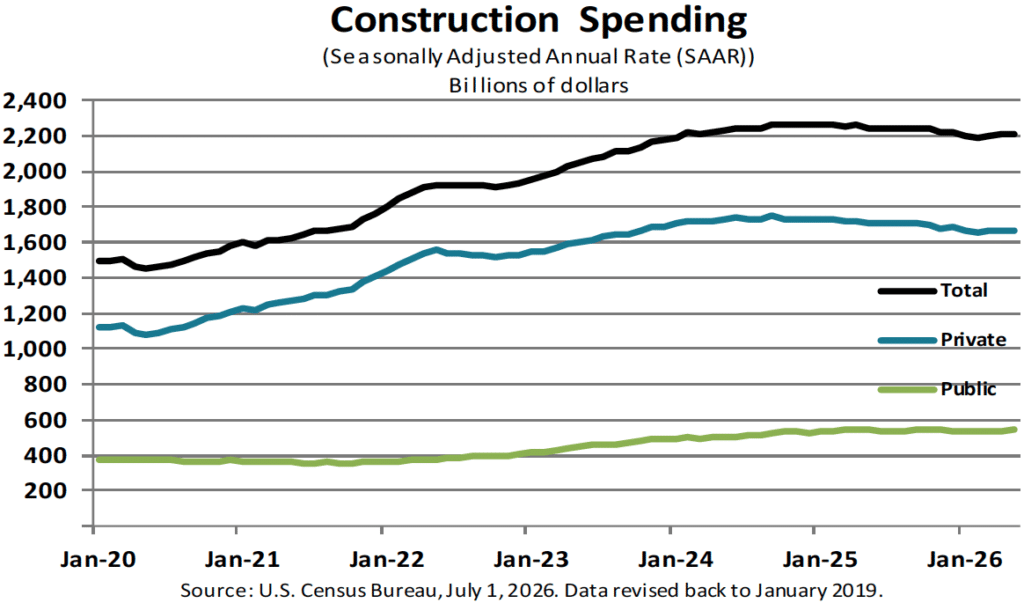

May private construction spending of $1.669 trillion was virtually unchanged from April and down 2.1% year-over-year, while public spending of $541.2 billion was up 0.5% month-to-month and up 0.3% year-over-year.

Total residential spending of $942.8 billion was up 0.4% month-to-month and 1.8% year-over-year, while total nonresidential spending of $1.267 trillion was virtually flat from April and down 3.8% year-over-year.

May nonresidential spending increased month-to-month in 11 of the Bureau’s 16 subcategories, led by religious construction at +1.6%, conservation and development at +1.4%, amusement and recreation at +0.9%, communication at +0.7% and highway and street at +0.6%. The largest monthly decline was in manufacturing, down 1.4%.

Private nonres construction fell for a seventh straight month and was down 6.6% year-over-year in May.

“This weakness is largely due to the ongoing decline in manufacturing-related construction spending as CHIPS Act-supported projects wind down, yet overall there are few sources of momentum in the segment,” Associated Builders and Contractors Chief Economist Anirban Basu said in the firm’s analysis of the May data. “Yes, the amusement and recreation category continues to grow at a healthy pace, and the religious category has rebounded meaningfully over the past year. But those modestly sized segments are far too small to carry the broader nonresidential market, especially given the weakness in larger categories. For instance, warehouse construction spending, which appeared to stabilize at the start of 2026, has now fallen for three consecutive months and is down 8.5% year over year, while the general office category remains in a state of freefall, down 11.9% since May 2025. For now, momentum remains largely concentrated in the data center segment.”

Private Construction — Residential vs. Nonres

Within May private construction spending, residential was up 0.3% month-to-month and nonresidential was down 0.3%, marking the eighth straight monthly decline for private nonresidential spending.

Private residential spending was up 1.8% year-over-year, while private nonresidential spending was down 6.6%. Within private nonresidential, spending fell in four of 11 subcategories: manufacturing, educational, commercial and power. Manufacturing continued to weigh on the segment, down 1.3% from April and 22.0% year-over-year.

Public Construction

Public construction remained a modest source of strength in May. Public nonresidential spending increased 0.4% from April and was up 0.3% year-over-year.

Within public nonresidential construction, spending increased in nine of 12 subcategories, was flat in commercial and declined in transportation and power. Educational construction — the largest public nonresidential subcategory besides highway and street — increased 0.6% month-to-month, while highway and street construction was also up 0.6%.

Related Posts

-

Solid housing construction spend more than offset a third straight private nonres decline. Get the…

-

October negated most of September's decline and was the fourth gain in the past five…

-

The topline figure snapped three straight months of decline, though nonresidential spending saw a sharp…