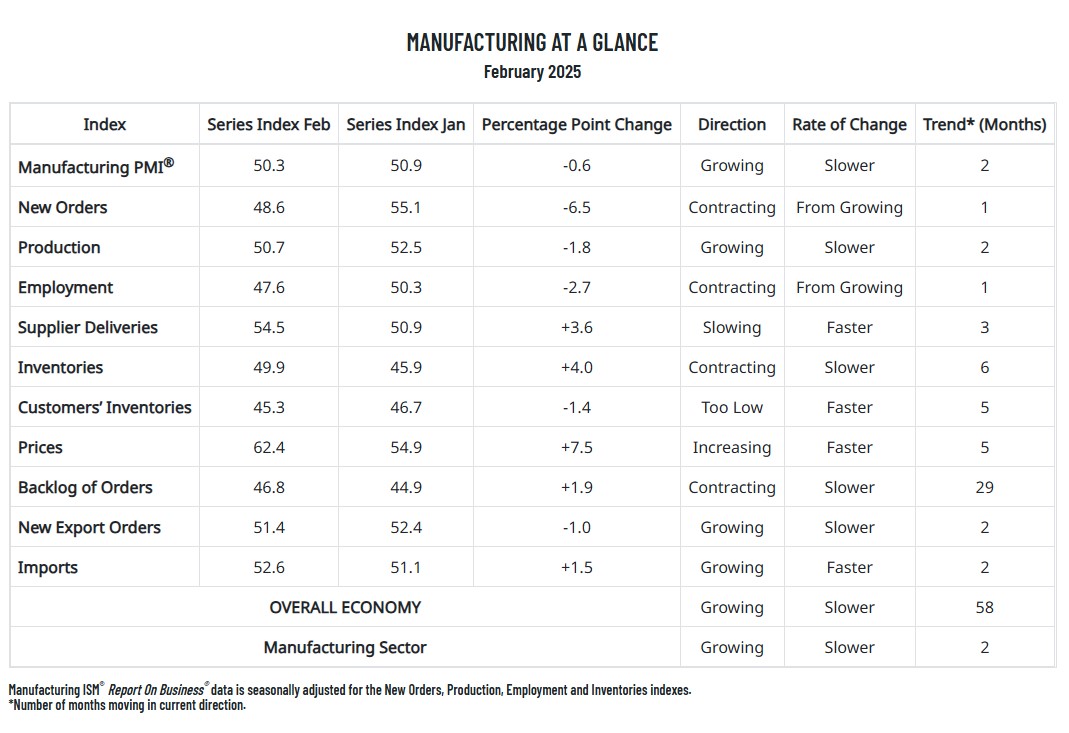

The Institute for Supply Management released its monthly manufacturing Purchasing Managers Index (PMI) on March 3, reflecting February activity, which revealed a moderate month-to-month decline overall, driven by a decline in the subindexes for production, while prices rose.

The PMI — regarded as a reliable indicator of overall U.S. industrial economic health — was down 0.6-percentage-points from January to a reading of 50.3%. January was the PMI”s first reading in expansion territory (50.0% or above) since March 2024 and its highest since October 2022. Following January’s 1.7-point increase, February’s reading indicated that activity expanded for a second consecutive month, though at a slower pace than January.

Trump: U.S. to Impose Another 10% Tariff on China (Feb. 28)

Economists surveyed by Reuters had predicted the PMI would rise to 50.5%.

More granularly, the latest report showed that demand weakened with new orders dropping into contraction territory, while production stabilized but remained lower than January’s performance (in expansion territory for second straight month) and inputs revealed the first signs of supplier difficulties in part due to some deliveries and discussions about who will pay for tariffs.

Tariff Watch: Implications and Strategies for Distributors Webcast (free upon registration)

source: tradingeconomics.com

Of the February PMI’s factoring indexes, four ended the month is contraction territory. The figure was driven by declines of 6.5 in new orders and 2.7 in employment, offset by increases of 7.5 in prices, 4.0 in inventories and 3.6 in supplier deliveries.

“Demand eased, production stabilized and destaffing continued as panelists’ companies experience the first operational shock of the new administration’s tariff policy,” ISM Manufacturing Business Survey Committee Chairman Timothy Fiore said in the institute’s March report. “Prices growth accelerated due to tariffs, causing new order placement backlogs, supplier delivery stoppages and manufacturing inventory impacts. Although tariffs do not go into force until mid-March, spot commodity prices have already risen about 20 percent.”

MDM’s 4Q24 MarketPulse Report (store link)

Fiore added that 24% of manufacturing GDP contracted in February, down from 43% in January. The share of sector GDP registering a composite PMI calculation at or below 45% — considered a good barometer of overall manufacturing weakness — was 2% in February, a 6-point improvement compared to January’s 8%.

The 10 manufacturing industries reporting growth in February were: Petroleum & Coal Products; Miscellaneous Manufacturing; Primary Metals; Wood Products; Food, Beverage & Tobacco Products; Electrical Equipment, Appliances & Components; Chemical Products; Plastics & Rubber Products; Fabricated Metal Products; and Transportation Equipment.

The five industries reporting contraction in February were: Furniture & Related Products; Textile Mills; Nonmetallic Mineral Products; Computer & Electronic Products; and Machinery.

Related Posts

-

Wholesale prices remained particularly elevated in January, driven by increases in both final demand and…

-

The company reported volume growth in key specialty product categories, while price deflation impacted overall…

-

The Consumer Price Index rose month-to-month and year-over-year, both surpassing expectations with increases in shelter,…