The impact of the Trump administration on demand and margins was the catalyst for a question in the 4Q24 Baird-MDM Distribution Survey, which polled nearly 300 respondents — U.S. and Canadian distributors being the vast majority — during early January 2025.

The broader theme of the results boiled down to “More demand, lower margins.”

Research: Distributors’ Top Concerns to Start 2025

Distributors are paying close attention to these tariff policies and how they will impact their revenue and margins in 2025, though the news cycle for it can lead to whiplash. The survey also collected write-in responses from about 150 respondents. The results showed that some distributors are concerned that tariffs could complicate supply chain planning, although others remain hopeful for a boost in demand.

Recurring Themes

After distilling the write-in responses, here are the biggest takeaways we had:

- Tariffs dominate concerns: Tariffs are expected to increase costs, impact margins and introduce significant uncertainty across industries. However, they also present opportunities for domestic production to gain a competitive edge.

- Deregulation and pro-business agenda drive optimism: The administration’s focus on deregulation and reducing business costs is viewed favorably, with expectations of increased demand in the long term

- Short-term pain, long-term potential: Businesses anticipate challenges like labor shortages, inflationary pressures and margin compression but remain cautiously optimistic about future growth

- Sector-specific nuances: While the outlook varies by industry, the construction, automotive and manufacturing sectors highlight the complexity of balancing demand, costs and margins

MDM’s 4Q24 MarketPulse Report (store link)

Demand vs. Margin Impact of Trump 2.0

On the qualitative side, here’s how respondents voted in regards to demand and margin impacts from President Trump’s second term:

Overall, respondents have mixed feelings about the impact of the administration on demand and margins, which is further illustrated in the charts below.

What Impact Do You Expect the Incoming Administration to Have on Demand?

A combined 54% of respondents answered that the administration would have a positive impact on demand vs. 25% responding negatively, indicating an overall positive expectation in 2025 for demand, while 21% indicated they expect no material impact on demand from the Trump administration’s trade/tariffs policy.

One respondent shared a positive perspective on the impact the administration could have on demand, saying, “Tariffs will potentially impact margins, but enterprise business demand is forecasted to be strong.”

Here’s the survey response to the second part of this question, which asked how they see the administration’s policies impacting profit margins:

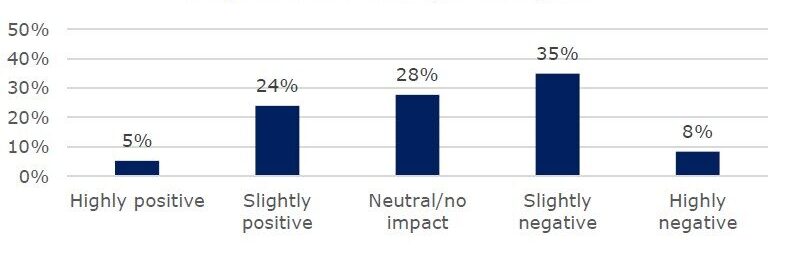

What Impact Do You Expect the Incoming Administration to Have on Margins?

As opposed to the demand question, only a combined 29% of respondents indicated that the incoming administration would positively affect margins vs. 43% who responded negatively, while 28% indicated they expect no material impact on margins from the Trump administration.

Go Deeper

The write-in responses showed considerable variation, especially among some Canadian distributors. One distributor from Canada said the possibility of a “tariff war” could negatively impact their business and raise costs from U.S.-based suppliers. Another alluded that margins, rather than the end consumer, would be affected, saying, “we expect a rebound in new construction-related demand; however, we also expect an increase in the cost of certain parts and consumables that will negatively impact margins as we don’t expect to be able to fully pass those cost increases onto the end consumer.”

Survey Commentary Key Themes and Takeaways

We distilled the analysis of those 150 write-in responses to these survey questions about tariffs policy into the following sentiment breakdown. Here are the key themes and takeaways identified:

1. Tariffs and Trade Policy

-

-

- Concerns about cost increases: Many respondents anticipate higher input costs due to tariffs on imported goods (e.g., steel, fasteners, building materials), which are expected to compress margins

- Mixed impact on domestic production: While some see potential benefits for domestic manufacturing due to reduced competition from imports, others fear negative effects on export sales

- Uncertainty and disruption: Tariffs are frequently cited as a source of unpredictability, making it difficult for businesses to plan their supply chain strategies

- Sectoral differences: Certain industries (e.g., automotive, construction) are particularly concerned about tariff impacts, with some expecting short-term pain and others projecting long-term gains

-

2. Demand Expectations

-

-

- Optimism for increased demand: Many respondents expect increased demand driven by pro-business policies, deregulation and onshoring initiatives. Sectors like oil and gas, construction and manufacturing are highlighted as likely beneficiaries

- Tariffs dampening demand: Higher consumer prices due to tariffs are expected to lower discretionary spending and reduce demand, particularly in price-sensitive markets

- Regional and sectoral variances: Canadian and Mexican businesses foresee negative impacts from tariffs and trade policy shifts, while U.S. manufacturers expect a boost in demand for locally made products

-

3. Margins Under Pressure

-

-

- Difficulty passing on costs: Respondents expressed concerns about being unable to fully transfer tariff-driven cost increases to customers, leading to compressed margins

- Labor shortages and immigration policy: Policies targeting undocumented immigrants are seen as potentially exacerbating labor shortages in trades, driving up costs and affecting project timelines

-

4. Pro-Business Sentiment

-

-

- Deregulation and tax reform: Many respondents view the administration’s deregulatory agenda and tax cuts as positive drivers for economic growth and business investment

- General optimism: A recurring theme is optimism about a favorable business climate, though tempered by concerns about the specific implementation of policies like tariffs

-

5. Uncertainty and Caution

-

-

- Short-term vs. long-term impacts: Many respondents expect short-term disruptions but are optimistic about potential long-term benefits from reshoring, reduced regulations, and increased domestic investment

- Wait-and-see approach: Uncertainty about the scale and timeline of policy changes leads some businesses to adopt a cautious stance, delaying investments or operational changes

-

6. Industry-Specific Observations

-

-

- Construction and building materials: Concerns about labor shortages and higher costs due to tariffs dominate. However, there is optimism for a rebound in construction demand

- Oil and gas: Positive outlooks are tied to deregulation and support for the energy sector

- Luxury goods and high-income markets: These segments are more optimistic, anticipating that tax breaks and consumer confidence will drive demand

-

Selected Commentary

Here is a selection of a dozen survey responses we found particularly interesting or well thought out that warranted sharing:

- “Tariff impact will likely reduce imports, which helps our domestic production business, but hurts our import lines.”

- “I believe that there are a couple basic factors influencing my response. First, tariffs have the potential to raise homeowners’ costs of necessary, daily, need purchases which will lower their discretionary income and potentially cause a fear of spending. Secondly, the deportation of undocumented immigrants will only further put strains on the trades needed to complete residential projects. Both these basic thoughts together will lead to a shrinking demand and a more price-sensitive competitive landscape for distributors.”

- “Higher than norm demand 1Q due to unknown tariff actions in Canada. If enacted, uncertainties with current U.S.-based supply chain versus optional offshore supply options exist.”

- “Historically, we have seen much better sales and margins under Republican administrations, and we saw immediate improvement last time under a Trump administration.”

- “Expect Demand to increase because of more favorable business climate, more confidence, but concerned tariffs will drag down greater Demand impact. Tariffs will temper both Demand and our Margins.”

- “We have major concerns over the impact of Tariffs from multiple countries, it is difficult to plan our global sourcing and supply strategy given current political comments.”

- “The President has no impact on our margins. I do expect the manufacturing economy will improve in time, due to reduced regulations and a more business-friendly administration. I have no concerns that tariffs will negatively impact inflation.”

- “Onshoring programs will benefit our strong OEM customer base. We are being told that quoting was extremely solid in 4Q24. Expectation is that orders will start to increase through 1Q25.”

- “We believe that policies focused on regulation pullback will spur demand and that from a margin perspective we will be able to pass on most product cost increases as we have in the past.”

- “I think energy prices will come down. This will hold inflation down. This will cause interest rates to drop. This will increase housing starts, all of which will help the wood products industry.”

- “We are a U.S. Domestic Manufacturer. Tariff threats or imposition will impact the supply chain for imported products. The Trump administration is supportive of domestic oil and gas industries. This will increase demand for pipe, valves and fittings.”

- “The incoming administration’s tariff threats could amount to a 25% tax on over 60% of the products we use and sell. When there is no domestic alternative available, tariffs punish only American businesses and consumers.”