The Institute for Supply Management released its monthly manufacturing Purchasing Managers Index (PMI) on Aug. 1, reflecting July U.S. industrial activity, which showed a deceleration to a 10-month low.

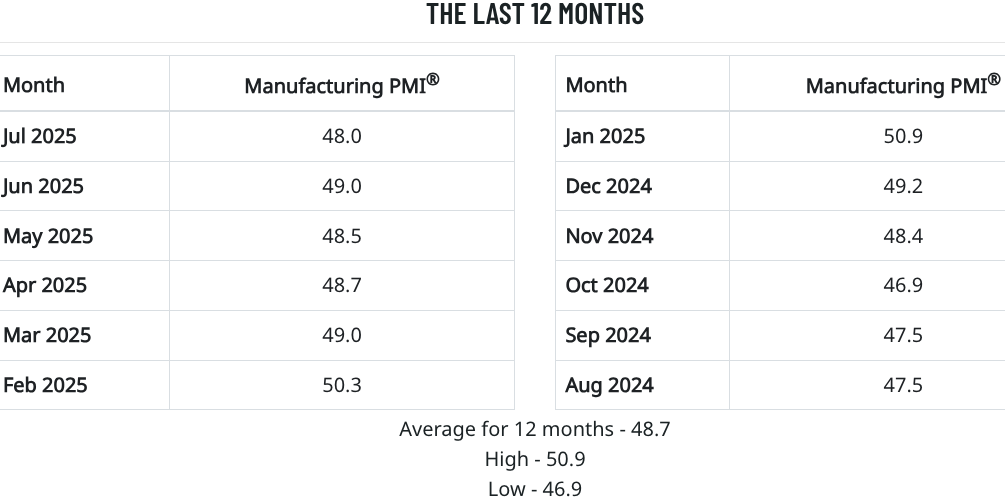

The PMI — regarded as a key of U.S. industrial health — was down one percentage point month-over-month to a reading of 48.0%, following a 0.5-point gain during June. It marked the fifth straight month that the PMI was in contraction territory (anything below 50.0%) after a brief expansion in January-February preceded by 26 months of contraction.

The PMI — regarded as a key of U.S. industrial health — was down one percentage point month-over-month to a reading of 48.0%, following a 0.5-point gain during June. It marked the fifth straight month that the PMI was in contraction territory (anything below 50.0%) after a brief expansion in January-February preceded by 26 months of contraction.

July’s reading was the PMI’s lowest since October 2024’s 46.9%

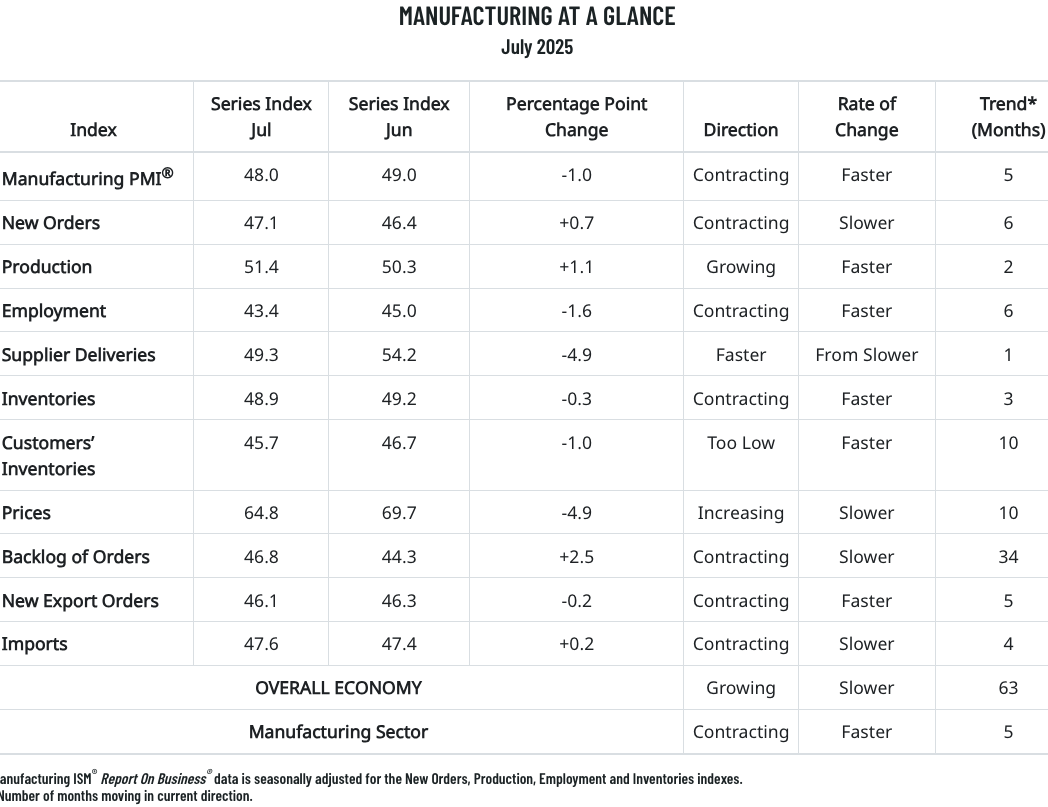

More granularly, the latest report showed that output revealed mixed results in July, with the PMI’s subindex for production up 1.1 points to 51.4%, while new exports declined 0.2 points, remaining in contraction territory at 46.2%. Reflecting slackening demand and tariff pricing, the imports index remained in contraction territory during July but increased 0.2 points to 47.6% after jumping 7.5 points in June. Meanwhile, the index for new orders contracted for a sixth month in a row, but increased 0.7 points to 27.1%, while prices sunk 4.9 points to 64.8%.

MDM’s 2Q25 MarketPulse Report (store link)

Of the five subindexes that directly factor into the PMI, one — production — was in expansion territory, down from two in June.

Here’s how the overall Manufacturing PMI has looked in bar chart form over the past 12 months:

source: tradingeconomics.com

Of the 17 manufacturing industries the PMI reflects, seven reported growth in July, led by Apparel, Leather & Allied Products and Plastics & Rubber Products The 10 industries reporting contraction were led by Printing & Related Support Activities and Paper Products.

In the Store: MDM’s U.S. MRO Market Trends Report

PMI Respondent Commentary

- “Fairly flat quarter over quarter, but with us being in the safety and security sector (and with U.S. Customs and Border Protection as a customer), the recent bill that passed should result in an increase in business in the coming months.” [Computer & Electronic Products]

- “Sales continue at unprecedented growth, driven by data-center construction. Customers and the sales team continue to demand lower pricing, which drives down gross margins in face of input price increases, primarily from aluminum imports.” [Chemical Products]

- “These tariff wars are beginning to wear us out. It’s been very difficult to forecast what we will pay in duties and calculate any cost savings we’ve had this year. Also, tariffs have disrupted our customs import bond. There is zero clarity about the future, and it’s been a difficult few months trying to figure out where everything is going to land and the impact on our business. So far, tremendous and unexpected costs have been incurred.” [Apparel, Leather & Allied Products]

- “Currently, higher interest rates still depress the construction industry for new construction projects. Tariff policies are uncertain, which slows down (1) our investment in new projects, (2) component sourcing for new products, (3) blanket orders and (4) replenishment of large inventory quantities. Instead, we’re working to shift suppliers to lower political risk countries or develop domestic sources. We are impacted by the higher tariffs on costs of raw materials and components both sourced domestically and from overseas, and we expect expenses will be higher in the third and fourth quarters as we consume the inventory received with new and higher tariffs or update costs from domestic sources in the second quarter.” [Machinery]

- “Sales softening more than usual during the summer. Negotiations with non-U.S. manufacturers are strained as we are reluctant to issue POs for deliveries three or more months into the future with prices that include current tariffs.” [Fabricated Metal Products]

- “In the health-care world we continue with ‘business as normal,’ but we are increasingly searching and assessing geopolitical risk mitigation options.” [Miscellaneous Manufacturing]

- “Tariffs are causing complete uncertainty around sourcing strategies. A sit-and-wait game for now.” [Electrical Equipment, Appliances & Components]

- “Sales are about on par with 2024, but nowhere near budget forecast. Tariff concerns seem to be growing as the year progresses.” [Nonmetallic Mineral Products]

- “Business is steady, with solid bookings and backlog. Still uncertainty about tariffs and associated inflation.” [Furniture & Related Products]

- “Energy capacity, specifically in the grid operated by PJM Interconnection, continues to be one of the major concerns for business continuity and growth in this region. The procurement of power and rising natural gas prices in this region due to past green energy policies, coupled with future projected allocations for artificial intelligence data centers, adds additional stress to the PJM system.” [Primary Metals]

- “Cautiously stable. Tariff impacts are still being monitored. Some increases have been implemented while monitoring other products.” [Transportation Equipment]

Related Posts

-

The overall reading remained in expansion territory after nine straight months of contraction that ended…

-

A new chair will succeed Timothy Fiore in June 2025 to lead ISM’s Manufacturing Business…

-

Following two consecutive months in expansion territory, March fell back into contraction and below economists'…