U.S. manufacturing health may be settling into a new normal.

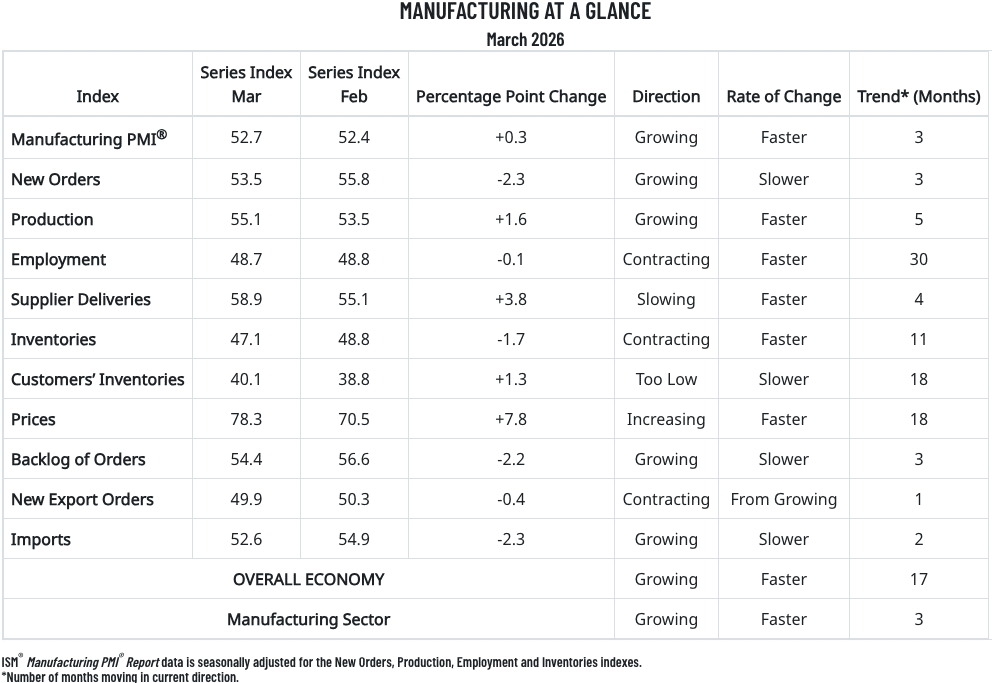

After hovering near the high end of contraction territory throughout most of 2024-2025, the Institute for Supply Management’s monthly manufacturing Purchasing Manager’s Index — seen as a reliable barometer for the industrial sector — recorded its third straight month of expansion in March, and its best mark since July 2023.

The PMI had held in the high-40s for two years before surging 470 basis points in January, and it’s held near there since.

The biggest driver of the recent PMI readings is pricing, with its subindex jumping another 780 bps in March to 78.3% — its highest reading since June 2022 and a 1,930-point jolt since January. Meanwhile, the new orders subindex fell 2.3 bps in March to 53.5% and the production index improved 160 bps to 55.1%.

ISM PMI March Survey Respondent Commentary

ISM noted that March marked the first monthly report in which survey panelists cited the Iran war as a new impact to their business, along with ongoing uncertainty with U.S. economic policy, despite the recent Supreme Court ruling striking down IEEPA tariffs. In March, 64% of overall comments were negative. Among the negative comments, about 20% cited tariffs and about 40% cited the Iran war.

Here is the sampling of commentary provided by ISM in its March manufacturing PMI report:

- “This is expected to be a transition year for the U.S. trucking market, with gradual stabilization driven by capacity tightening and replacement demand instead of growth. Demand should stay constrained by weak carrier profitability and high equipment costs but improve modestly late in the year.” [Transportation Equipment]

- “Changes in the tariff structure are bringing cautious opportunities to offset significant costs for the balance of 2026. The actions in Iran, however, add a new wrinkle to energy costs throughout the world, including India. We continue to try and plan for the unpredictable and unexpected.” [Transportation Equipment]

- “We’re seeing steady increases in activity, but geopolitical issues and the Iran war are already waning sentiment.” [Fabricated Metal Products]

- “Customer orders have increased considerably as the construction market remains strong, resulting in higher production volume and increased forecasts to suppliers.” [Machinery]

- “Current Middle East unrest is already starting to impact business operations by increasing lead times, costs, container delays and the like.” [Food, Beverage & Tobacco Products]

- “Lots of relief from Supreme Court striking down (emergency) tariffs, particularly with organic cane sugar from Brazil.” [Food, Beverage & Tobacco Products]

- “Geopolitical tensions related to the conflict in Iran are contributing to rising manufacturing supply costs, and ongoing tariff uncertainty is negatively impacting purchasing strategies and cost forecasts.” [Chemical Products]

- “Ongoing geopolitical instability has emerged as a persistent factor influencing global trade dynamics. We anticipate strategic realignment of supply chains as organizations respond to energy market volatility and shifting trade policies. In light of these macroeconomic headwinds, we — like most organizations — are maintaining a cautious posture regarding investment commitments while continuing to monitor market conditions closely. Our purchasing strategy is being recalibrated to address supply chain vulnerabilities exposed by energy market volatility and evolving trade protectionism.” [Chemical Products]

- “Metal commodity prices continue to put pressure on mechanical commodities. Memory price escalation is causing large cost increases that cannot be mitigated in other areas of the product cost.” [Computer & Electronic Products]

- “The Middle East war has created domestic and global turmoil for the olefins and polyolefins business. Feedstocks and finished product pricing are accelerating dramatically as Middle Eastern and Asian producers suffer from shipping blockages. Global customers for packaging resins are scrambling to cover needs from North America and South America in the face of supply chain complications.” [Plastics & Rubber Products]

Related Posts

-

October's decline negated September's gain, as weakness in production more than offset modest gains in…

-

It marked the 10th straight month that the PMI has been in contraction, and the…

-

ISM shared that 19% of the manufacturing sector’s GDP contracted in April, compared to 16%…