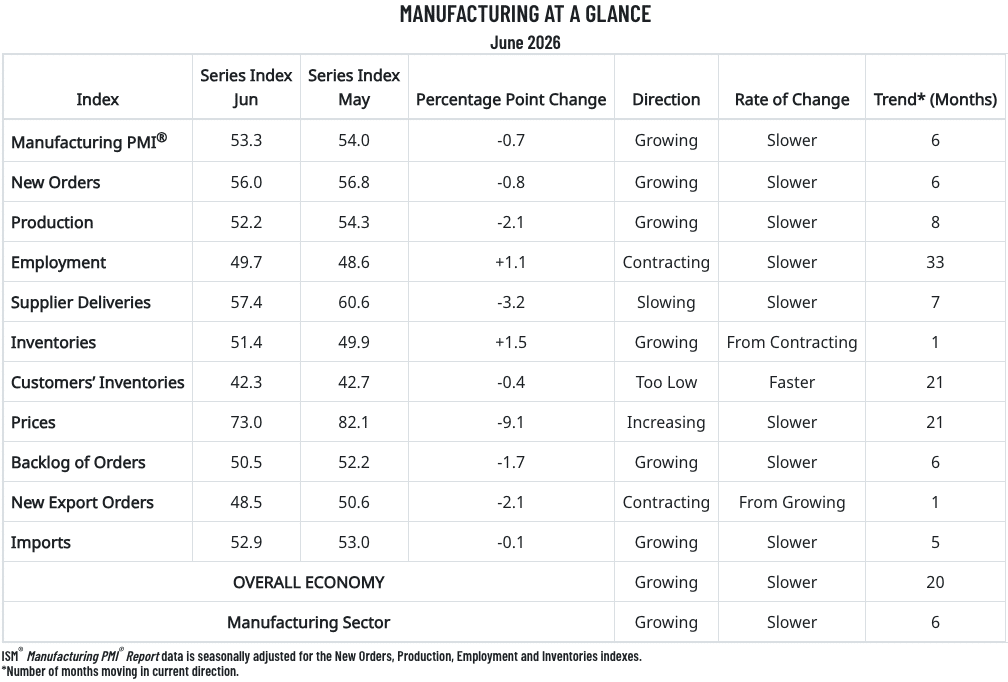

U.S. manufacturing activity decelerated in June after notching a three-year growth peak in June, according to the latest Purchasing Managers Index from the Institute for Supply Management, published July 1.

Seen as a reliable barometer for the industrial sector, the PMI registered 53.3% in June, down 0.7 percentage points from May. It marked the PMI’s first monthly decline since January.

Consensus market expectations were for the PMI to hold steady or dip by 0.1 percentage point.

Of the five core subindexes that comprise the PMI, the ones for New Order and Production decelerated, while Supplier Deliveries — the only subindex that is inverted (anything above 50% indicated slower deliveries) — indicated slowing performance for a seventh straight month and by a slower rate than May. Within the other five subindexes, Prices slowed by 9.1 percentage points for its second straight deceleration after peaking at 84.6% in April.

ISM shared that 5% of the manufacturing sector’s GDP contracted in June, compared to 2% in May, and the percentage of GDP in strong contraction (composite PMI of 45% or lower) was 3% — vs. 2% in May and April.

All but one (Petroleum & Coal) of the six largest manufacturing industries expanded in June, in the order of Computer & Electronics; Machinery; Transportation Equipment; Chemicals; and Food, Beverage & Tobacco.

ISM PMI May Survey Respondent Commentary

In the June survey commentary collected by the ISM, 34% of comments were positive and 66% negative — an improvement from 25%/69% in May. Among negative comments, the Iran war was mentioned in 31% and tariffs in 17%, ISM noted, while 50% of panelists mentioned pricing volatility as an issue for their company.

Here is a sampling of commentary provided by ISM in its June manufacturing PMI report:

- “The conflict in Iran has impacted pricing in every category of raw materials. Especially, items that have a heavy concentration of oil in the components like our adhesives.” [Chemical Products]

- “Continued pressure from conflict in Middle East is resulting in a more conservative approach to capital expenditures. We are seeing an increase in consumables and services purchasing from sectors like chemical analysis, per- and polyfluoroalkyl substances (PFAS), and environmental and pharmaceutical testing.” [Computer & Electronic Products]

- “General purchasing operations are being shaped by (1) moderating but still elevated inflation, (2) higher interest rates and (3) continued policy uncertainty, particularly around tariffs and global trade. While overall economic growth remains resilient, it is slowing as consumer spending weakens under pressure from higher costs for energy and essential goods, reducing demand visibility and increasing cost sensitivity for buyers. Meanwhile, supply chains have stabilized compared to prior years but remain structurally complex, with trade policy volatility, geopolitical tensions and regulatory changes now ongoing cost drivers rather than temporary disruptions. Our organization continues balancing cost control with resilience, shifting sourcing strategies, tightening inventories and prioritizing supplier diversification and risk management.” [Computer & Electronic Products]

- “Retail electronics sales seem to have stabilized to some extent. The pause in tariff changes has been welcomed the last two months, but it’s only a matter of time before more confusion is introduced.” [Electrical Equipment, Appliances & Components]

- “Input costs remain elevated across key categories, driven largely by Middle East conflict impacts and ongoing tariff uncertainty. Supplier lead times have stretched, which is influencing our inventory strategy and sourcing decisions. We are managing exposure through diversified supplier bases and contract structures that balance cost certainty with operational flexibility.” [Food, Beverage & Tobacco Products]

- “Conditions are optimistic but not yet booming for our company, even though many others, it seems, are experiencing growth. Machinery in support of defense and semiconductor manufacturing is very strong, a bright spot for our team. Industrial and medical clients are slow to purchase, focusing more on refurbished and upgraded units versus new ones.” [Machinery]

- “Core business remains solid in the face of ongoing geopolitical uncertainty. Cautiously optimistic that a deal will be reached to reopen the Strait of Hormuz; concerned about ongoing ripple effects even when the strait reopens but situation is highly concerning if the strait remains closed. AI industry continues to have huge capacity consumption for critical electronics. Monitoring impact of U.S. defense industry needs on supplier capacity.” [Miscellaneous Manufacturing]

- “No major changes from last month. With the potential ending of the Iran war, management is expecting us to go back to February pricing structures and plans since the increase in oil prices was driven by the war and not regular market influences.” [Petroleum & Coal Products]

- “Requests from suppliers in Europe and India for ‘energy surcharges’ have stopped this past month. We’re seeing continued capacity growth in the Asia-Pacific region (excluding China), including Vietnam, Thailand and South Korea. Most suppliers are building for the longer term as geopolitical protection from all sides.” [Transportation Equipment]

- “The new Section 232 tariffs continue to destroy our profitability and demand as we have to raise prices to deal with this gigantic tax. Add the ‘incentives’ for our company to pivot to purchasing non-U.S. sourced material, and one realizes the total ineptitude of this tariff policy.” [Transportation Equipment]