The Institute for Supply Management released its monthly manufacturing Purchasing Managers Index on March 2, reflecting February U.S. industrial activity, which indicated a modest regression after January marked a long-awaited return to expansion territory and the PMI’s largest jump in 4 years.

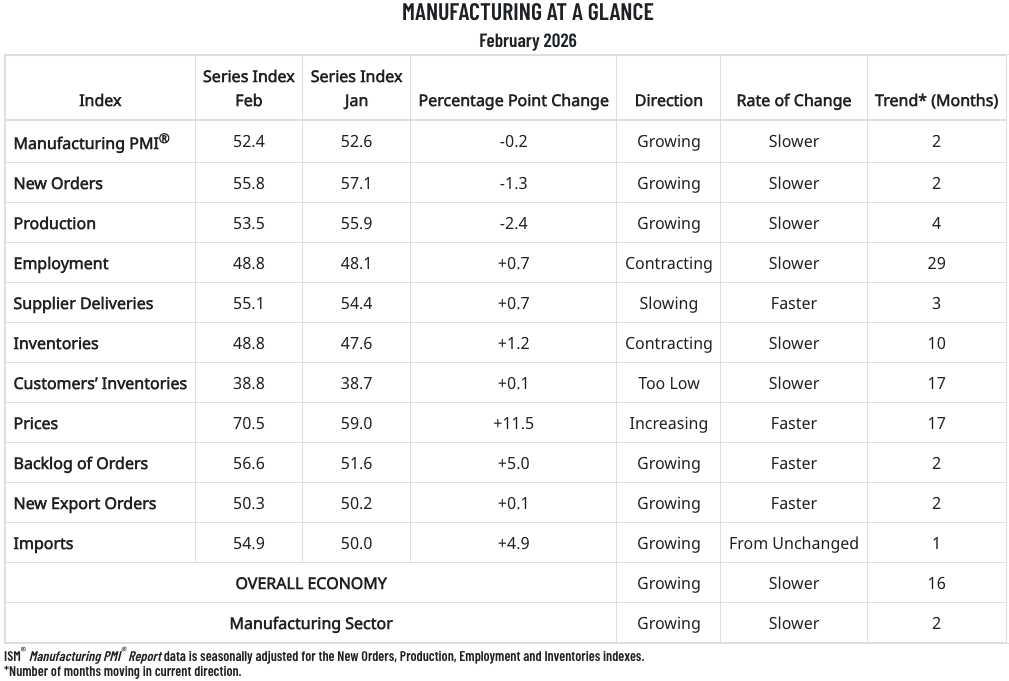

The PMI — regarded as a key indicator of U.S. manufacturing health — showed a February reading of 52.4%, down 0.2 percentage points from January and topping economists’ expectations of 51.8%. It was the second straight month the PMI was in expansion (50.0% or better) after 12 straight months in contraction.

The narrow overall February decrease suggests sustained early-year momentum for U.S. manufacturing given that January reordering was likely at least partially responsible for that month’s major gain.

ISM’s February PMI report was led by slowdowns in indexes for New Orders (-1.3 points to 55.8%) and Production (-2.4 to 53.5%), though both remained in expansion. All other subindexes improved — most notably with Prices jumping 11.5 points to 70.5% for its highest reading since June 2022 (78.5%). Backlog of Orders (+5.0 to 56.6%) and Imports (+4.9 to 50.0%) also both had sizable increases.

The ISM report noted that 12 of the manufacturing sector’s 17 industries reported growth in February, compared to nine in January. Meanwhile, the report said 21% of the sector’s GDP contracted in February, holding steady with 20% in January and far below the 85% in December. Of the six largest industries, four expanded in February (five in January).

February ISM PMI Respondent Commentary

- “Today, American produced commodities like steel and aluminum are the highest priced in the world, by far. Hence, the Section 232 tariff policy is having the exact opposite effect of their intention on an American manufacturer like us: It is raising prices while lowering demand and profitability.” [Transportation Equipment]

- “Economic activity seems to be also challenging for this year. Some recovery in certain sectors in the economy but still lot of cost pressures and soft demand. Cost discipline is the priority.” [Chemical Products]

- “January sales continued to provide positive indications for growth opportunities. Data center, health care, and food and beverages remain positive growth areas. We continue to receive price increase notifications from suppliers based on unsupported tariff claims and are expanding corporate staff to support sales growth.” [Chemical Products]

- “South American instability has begun to be a factor for our suppliers and inventory management.” [Petroleum & Coal Products]

- “Pricing for outside purchases has stabilized. We are spending significant effort to work with our supply base to mitigate tariff impacts. Backlog is at a healthy level.” [Miscellaneous Manufacturing]

- “Overall orders and supply footprint are improving. As we review customer demand, we are also taking several categories of established materials and supplies out to RFP for review and cost improvements — in particular, printed circuit assemblies, plastics, sheet metal assemblies and motorized assemblies. This will help ease the burden of tariff and customer impacts as we broaden our supplier base to a more regional footprint.” [Computer & Electronic Products]

- “Continue to be impacted by tariffs. Seeing metals prices rise too. Business is steady, but domestic growth is slower than expected.” [Computer & Electronic Products]

- “Business was slow in January. Many orders pulled into end of 2025 to meet revenue goals. Order book is strong going forward.” [Electrical Equipment, Appliances & Components]

- “Tariff policy changes affect total acquisition costs and purchasing source decisions. So far this year, tariff instability still exists. Due to the tariffs, most raw materials used in manufacturing, such as steel and wire, need to be sourced domestically, and the cost keeps going up.” [Machinery]

- “Business is improving by the week. Backlog is growing, and new opportunities are everywhere. Monthly shipments are still lower than planned, but improving. Over the past five years, we spent thousands trying to attract new employees and had almost zero responses. In the last six months, however, we’ve been able to hire experienced engineers, computer numerical control (CNC) operators, and young people wanting to become CNC machinists.” [Fabricated Metal Products]

Related Posts

-

September's PMI rose slightly to 49.1% but stayed in contraction territory as some manufacturers report…

-

It marked the 10th straight month that the PMI has been in contraction, and the…

-

ISM shared that 19% of the manufacturing sector’s GDP contracted in April, compared to 16%…