Editor’s Note: This article’s author, Kevin Reid-Morris, is the founder of Veranda AI and was the lead researcher on NAW’s newly-published “In Search of Value: Where 400+ Distributors are Investing in AI Today” report — the findings of which will be presented at our SHIFT Conference May 12-14 in Denver. Join us there!

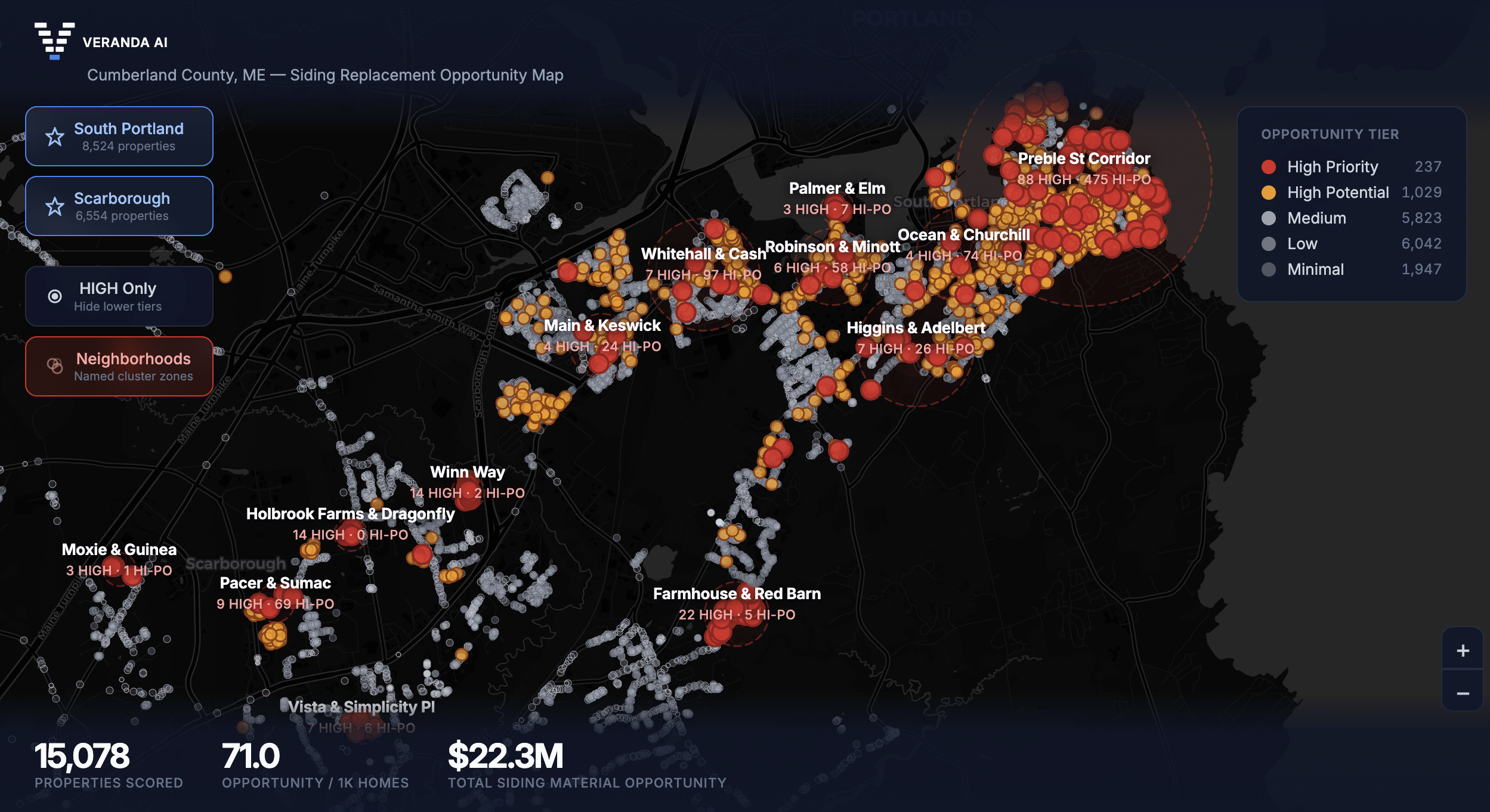

In late 2025, a series of AI agents went to work scanning 15,072 homes in one county in Maine. They gathered publicly available images, identified the siding material, assessed condition, flagged deterioration patterns and scored every property based on product replacement need, financial capacity and motivation to buy. Another set of agents developed visualizations of how high-scoring homes would look with all new siding and trim, placed on outreach materials personalized for each homeowner.

The whole process took hours, not months. The agents found 1,281 homes that scored as high-priority for siding replacement, making up $22.3 million in opportunity no manufacturer, distributor or dealer could see — all in one county, for one product category.¹

Not a single sales rep drove a mile. No one knocked on a door.

Finding a Data Desert

That kind of intelligence has never existed in building supply companies, at least for existing buildings. For new construction, deep databases have been available for decades. Larger firms routinely pay mid-six figures a year for data on housing starts and developer applications. But for every new home built in North America, over 100 homes are already standing.² And for the 99% of the market that is replacements, retrofits and renovations, there’s been a data desert for as long as anyone in the industry can remember.

Without intelligence or data, building supply companies have plodded along with trade shows, door knocking and spray-and-pray marketing. And this reliance on the same methods used for over a century have started to show up on the P&L. In an analysis of publicly listed building products companies, we were shocked to find that SG&A has climbed nearly 20% faster than revenue over the past 10 years.³ In other words, every dollar invested is producing less and less revenue.

Enter AI for distributors and manufacturers. The sector’s instinct has been to point AI at sales efficiency, leading to faster order entry, smarter routing and cleaner ERPs. While massively valuable, these efforts all rest on the same assumption: a customer has already decided to buy something. The front end of the funnel, though — like finding or creating an opportunity before they’ve called anyone else, remains almost completely unaddressed.

Beyond Boots on the Ground

It’s not for lack of trying. One major supplier we spoke with, determined to create demand and overcome the issue of contractors substituting lower-cost alternatives from competitors before they could even get involved, ran a herculean door-to-door canvassing program in a handful of markets to get there first. Boots on the ground in every territory had reps knocking on doors, assessing homes from the curb, pitching replacements on the spot and leaving door tags at every property of interest. While the results in these neighborhoods were spectacular — 4x increase in RFQs and a 70% sales lift — to pull it off in every territory just wasn’t scalable or viable.

I tried to solve this problem myself when working in building materials. Our teams scraped then-fuzzy satellite images, shipped them to offshore teams, manually compiled lists and handed them to sales reps who were terrific at closing inbound demand but had no idea how to be effective hunters. In the territories where we pieced it together, quoting activity jumped by an order of magnitude. But the process was impossible to sustain.

The insight worked: if only we had a way to structure, see and sort through the unstructured treasure trove of data out there on existing homes. The workflows didn’t scale. We eventually stopped.

Why the Moment is Now

What made our Maine agentic analysis possible is a convergence. Americans are staying in their homes nearly 12 years now, double the rate two decades ago, and they’re investing accordingly — spending on roofing, windows and doors has tripled since 2001.4 The median U.S. home is now 44 years old, meaning millions of exteriors are past their useful life. Meanwhile, manufacturers and distributors are hungrier than ever to innovate how they go to market, with sales channels cited as the single biggest threat keeping building supply executives up at night.5 And least of all, a seismic technological shift: machine vision and AI can now autonomously assess large volumes of data, including imagery, on every home’s exterior in any market with expert-level accuracy at a fraction of what it once cost in time and money. What my team used to do by hand is now autonomous, scalable and smarter.

Altogether, it means building supply leaders are no longer constrained by yesterday’s channels and data, or lack thereof. Instead, they’re setting out to flip the hundred-year-old orthodoxies of how they create — not just respond to — demand.

Right now, across your territories, there are millions of existing homes that require your building supplies. You just can’t see them yet.

[1] Analysis conducted by the author using AI-driven property scoring across South Portland and Scarborough, ME. Material opportunity calculated at manufacturer list pricing for engineered and premium siding products. Leads scored on exterior condition, homeowner financial capacity, and neighborhood renovation activity.

[2] Author’s calculation. U.S. Census Bureau estimates 148.7 million housing units (Q4 2025); Statistics Canada reports 17.2 million dwellings (2024). Combined ~166 million existing homes versus ~1.55 million North American housing starts annually.

[3] Based on 10-K filings of publicly listed building products companies including James Hardie, Trex, Masco, AZEK, and JELD-WEN, 2014–2024.

[4] Redfin, 2024 (median homeowner tenure: 11.9 years, up from 6.5 years in 2005); Joint Center for Housing Studies of Harvard University (spending on roofing, HVAC, windows, and doors tripled from 2001 to 2021); U.S. Census Bureau, American Community Survey 1-Year Estimates, 2024 (median home age: 43 years).

[5] McKinsey & Company, “Building products in the digital age: It’s hard to ‘get smart,’” June 2022. Global survey of 547 building products executives. Channel management scored as the highest-rated digital threat across all categories.

Related Posts

-

It adds two Gulf Coast locations to Hartmann's footprint.

-

The addition nets BFS its first two truss and wall panel facilities in the state…

-

Adding five facilities and 220 employees, the news came just two days after SRS announced…