The Institute for Supply Management (ISM) released its monthly Manufacturing ISM Report on Business on Sept. 1, and the well-regarded industrial economic barometer showed a second-straight improvement, though it remains in contraction territory.

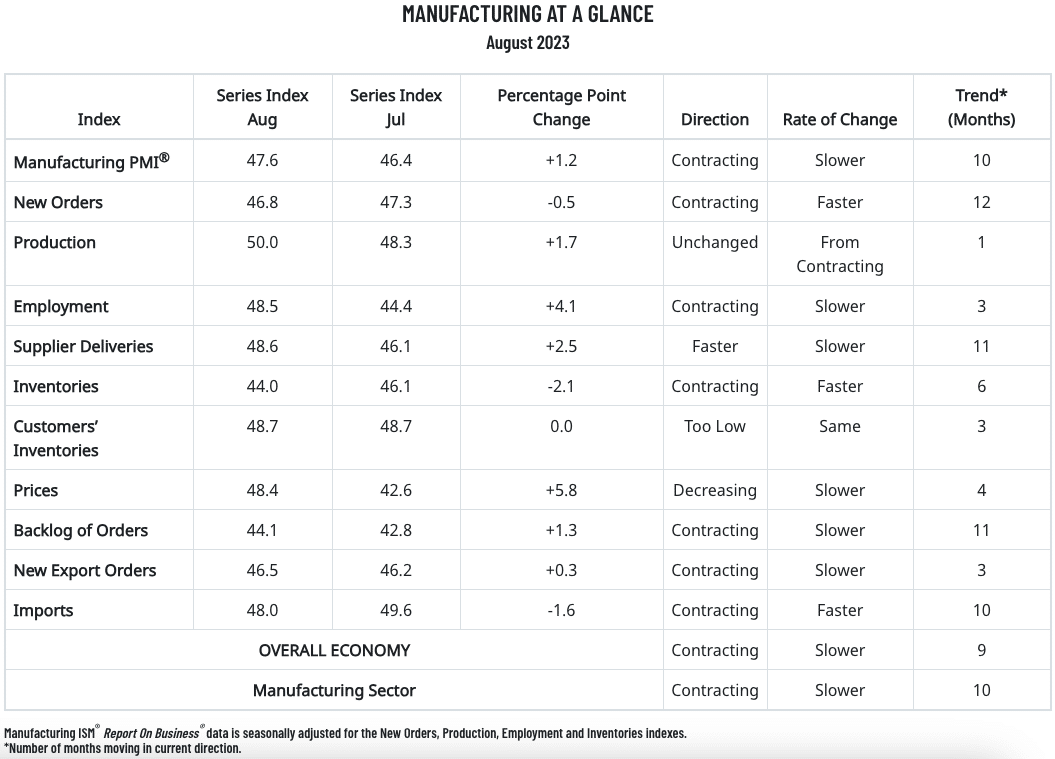

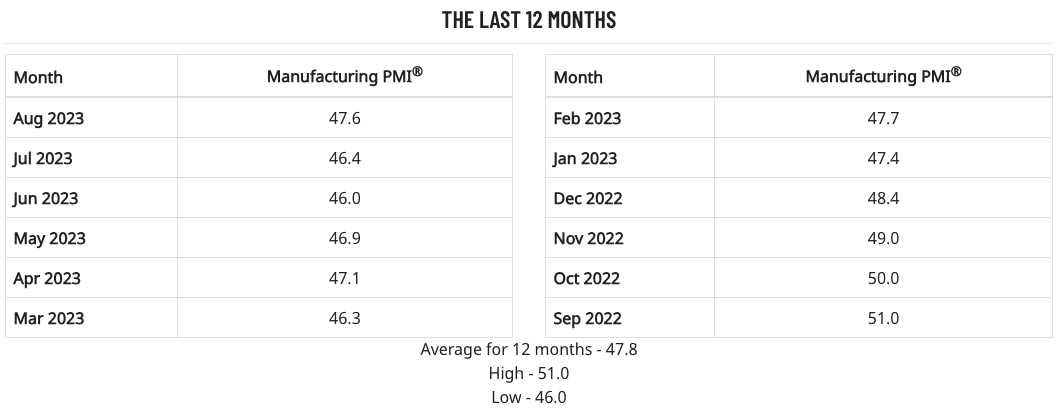

ISM’s August Producer Manufacturing Index (PMI) showed a reading of 47.6%, a 1.2 percentage point improvement from July, which had increased by 0.4 points from June. It was the 10th straight month that the PMI was in contraction (anything below 50.0%), following a 28-month streak of expansion coming out of COVID-19 pandemic-driven industry shutdowns.

MDM’S SHIFT | The Future of Distribution conference, held Sept. 18-20 in Denver, brings together distribution leaders to learn and network across topics of sales & marketing, digital transformation, data analytics and talent management. Find more info here.

Of the five subindexes that directly factor into the PMI, four were in contraction territory and one was flat at 50.0%. While those key subindexes were still in the negative, four of them saw healthy month-to-month growth:

- The New Orders Index dipped 0.5 points from July to 46.8%

- The Production Index reading of 50.0% was a 1.7-point increase from July

- The Prices Index jumped 5.8 points from July to 48.4%

- The Backlog of Orders Index increased 1.3 points from July to 44.1%

- The Employment Index increased 4.1 points from July to 48.5%

Meanwhile, the Suppliers Deliveries Index increased 2.5 points to 48.6% — it’s highest mark in the past 11 months. That index is the only one that is inversed, as a reading of above 50.0% indicates slower deliveries (which is typical as the economy improves and customer demand increases). Additionally, the Inventories Index fell by 2.1 points to 44.0%; the New Export Orders Index ticked up 0.3 points to 46.5%; and the Imports Index fell 1.6 points to 48.0%.

“The U.S. manufacturing sector shrank again, but the uptick in the PMI indicates a slower rate of contraction,” commented Timothy Fiore, Chair of ISM’s Manufacturing Business Survey Committee, in a news release. “The August composite index reading reflects companies managing outputs appropriately as order softness continues, but the month-over-month increase is a sign of improvement.”

Of the six biggest manufacturing industries factored in, three — transportation equipment; food, beverage & tobacco products; and petroleum & coal products — registered growth in August. That follows just one top industry — petroleum & coal products — that saw growth in July.

Here is a sampling of ISM manufacturing PMI survey respondent commentary for August:

- “Further reductions in customer orders due to the economic situation and also their working down of own inventories. Backlog is dwindling, but still showing robust revenue.” [Computer & Electronic Products]

- “Demand still weak. Customer inventories are getting depleted; however, we are not seeing a real uptick in demand. General supply conditions are softening.” [Chemical Products]

- “Still seeing a slowdown in orders. We’re continuing to ship to max capacity, with supply constraints still a real part of our day-to-day business operations.” [Transportation Equipment]

- “Customer orders have softened. This is likely due to customers’ increased confidence in the supply chain, (which) has them reducing their inventories. Customers are also being pinched with higher interest rates. Additionally, consumers are feeling their purchasing power eroded by stubbornly high inflation, so they are purchasing less.” [Food, Beverage & Tobacco Products]

- “Fourth quarter orders falling short of projection and indicating a slowdown in customer demand, though the first quarter forecast remains solid. Unclear if this is an inventory correction. Logistics stabilized and costs are matching 2019. Shortages limited to only a few items now, but suppliers are hesitant to add or replace labor needed in light of slowing demand.” [Fabricated Metal Products]

- “General slowdown in business at the end of the third quarter. For capital equipment additions, our customers are buying only what they need for specific jobs and not adding any capital fleet material for potential future work.” [Machinery]

- “There is additional softening in the market. Customers are hesitant to provide extended forecasts with today’s economic uncertainty.” [Electrical Equipment, Appliances & Components]

- “Business continues to remain strong with sales and profits both ahead of plan. The bookings were below what we planned, but that was expected due to fewer working days and summer vacations.” [Miscellaneous Manufacturing]

- “The manufacturing sector continues to be slow, and the low market prices make it difficult to stay profitable. On the positive side, laborers are showing enthusiastic employment interest. Rising energy and fuel prices are of concern to our company.” [Paper Products]

- “Business is beginning to improve moderately. Still well below 2022 levels, but it appears that the ‘great inventory rebalancing’ is finally coming to fruition.” [Plastics & Rubber Products]

- “Automotive volume remains strong in preparation for the United Auto Workers’ potential strike at Ford, General Motors and Stellantis. Contingency plans in place for sub-tiers. Continue to have issues recruiting general labor employees. Operational efficiency suffering due to a lack of human resources. Order book remains strong and ahead of 2022.” [Primary Metals]

- “(The Federal Reserve’s) actions to increase borrowing costs has dampened demand for residential investment. Recently, this slowdown plateaued somewhat, with demand stabilizing. The outlook for 2024 remains uncertain, and we continue to be cautious about building inventories.” [Wood Products]

Related Posts

-

For a second straight month, none of the PMI's 10 subindexes registered monthly expansion.

-

The official manufacturing purchasing managers’ index (PMI) was 49.3 in July, data from the National…

-

The Institute for Supply Management’s monthly Purchasing Managers Index (PMI) remained in contraction territory for…