The Big Picture

-

- It’ll be QXO’s third deal since its mid-2024 launch and early 2025 public trading debut, following Beacon (mid-2025) and Kodiak Building Partners (February 2026)

- In terms of purchase price, it’s second only to The Home Depot’s $18.25 billion acquisition of SRS Distribution as the largest deal ever inked in building materials distribution

- QXO states the move will position it as the second-largest publicly-traded building materials distributor by annual revenue (approximately $18 billion)

- It further rounds out QXO’s product offering with roofing (Beacon); lumber, construction supplies and millwork (Kodiak); and insulation (TopBuild)

QXO is making its boldest move yet in building materials distribution, announcing April 19 that it has reached an agreement to acquire insulation distributor and installer TopBuild for $17 billion — one of the largest transactions the durable goods distribution landscape has ever seen.

Our 2026 SHIFT Conference is coming May 12-14. Join us in Denver!

Unanimously approved by both companies’ boards and expected to close during 3Q26, the deal values TopBuild at roughly 14.9x expected 2025 EBITDA pre-synergies and 11.8x post-synergies, with about $300 million in expected cost and revenue synergies.

In comparison, that premium paid by QXO is notably less than the ~17x paid by The Home Depot for SRS. The transaction values TopBuild at $505 per share, whereas TopBuild’s stock traded as high as $550 in mid-February.

The acquisition is expected to be immediately and substantially accretive to earnings and materially expand QXO’s margins, according to the company.

“Over the past 11 months, we’ve built QXO into a market leader through more than $13 billion of acquisitions, closing on Beacon in 2025 and Kodiak earlier this month,” said QXO CEO Brad Jacobs, who stepped down from his Chairman roles at 3PL companies XPO and GXO at the end of 2025 to focus on QXO. “The TopBuild transaction will also give us critical mass in the insulation sector and expand our exposure to large, complex projects like data centers, where scale matters.”

A Transformational Leap for QXO

With the addition of TopBuild — alongside its recent acquisitions of Beacon (for $11B in mid-2025) and Kodiak Building Partners (for $2.25B in February) — QXO will emerge as the second-largest publicly traded building products distributor in North America, with more than $18 billion in combined revenue and over $2 billion in adjusted EBITDA.

That trajectory is striking given QXO only launched in mid-2024 and went public in January 2025. In less than a year, the company has gone from zero revenue and EBITDA in the sector to a scaled, multi-category platform with leadership positions across key segments.

QXO said that, once the TopBuild deal is complete, it will hold:

- No. 1 position in insulation

- No. 2 in roofing

- No. 1 in waterproofing

- Top-tier positions across lumber and broader building materials markets

The TopBuild acquisition alone expands QXO’s addressable market to more than $300 billion and significantly increases its exposure to large, complex commercial and industrial projects — including high-growth areas like data centers.

The combined company is expected to operate roughly 1,150 branches with about 28,000 employees and a fleet size of more than 10,000 vehicles.

“TopBuild has a deep bench of best-in-class operators, reflected in its industry-leading adjusted EBITDA margin of approximately 18%,” Jacobs continued. “We plan to replicate their best practices across QXO, including deploying their ‘special OPS’ teams to continuously improve operational excellence and customer service.”

TopBuild: Scale, Services and Diversification

TopBuild brings a differentiated model that blends distribution with installation services — a combination that has driven both growth and margin resilience.

TopBuild Fast Facts:

- Founded in 2015 upon its spin-off from Masco Corp., and debuted on the NYSE that same year

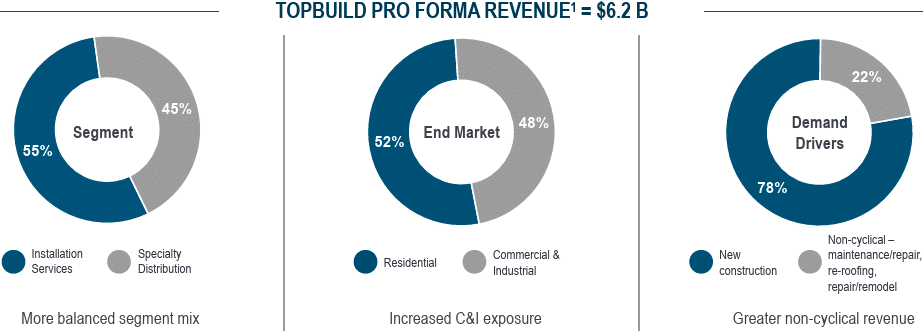

- Approximately $5.4 billion in 2025 revenue, with a pro forma run-rate above $6 billion when factoring in acquisitions, and adjusted EBITDA of roughly $1.0-$1.15 billion based on its 2026 outlook. In February, TopBuild forecasted 2026 annual sales of $5.925 billion to $6.225 billion.

- Headquartered in Daytona Beach, FL

- Business segments:

- Installation services — 55% of revenue (TruTeam, Progressive Roofing), delivering insulation and related installation work. 200+ branches throughout the U.S. and Canada.

- Specialty distribution — 45% of revenue (Service Partners, Distribution International), supplying insulation and mechanical systems products. 250+ branches across the U.S. and Canada.

- TopBuild is led by CEO Robert Buck. In early April, the company announced that John Achille was promoted to President alongside his role of COO.

- TopBuild completed seven acquisitions during 2025, totaling approximately $1.2 billion in added revenue. In 2026, it completed acquisitions of Applied Coatings and Upstate Spray Foam (both in Winfield, NY; $20M combined revenue) in February and announced another for Johnson Roofing (Waco, TX; $29M revenue).

- TopBuild acquired Specialty Products and Insulation (SPI) in October 2025 for $1 billion after the two companies previously nixed a deal agreement in April 2024 upon regulatory complications

TopBuild’s distribution and installation segment mix creates a balanced exposure between residential (52%) and commercial (48%) end markets, with about 52% tied to commercial and industrial activity and 22% of revenue considered non-cyclical (repair/remodel and maintenance).

Despite ongoing softness in residential construction, TopBuild has maintained strong profitability — with adjusted EBITDA margins near 18% in 4Q25 — supported by growth in commercial and industrial demand and disciplined execution.

“We’re excited to join QXO and combine our leadership in insulation installation and specialty distribution with QXO’s scale, technology, and procurement capabilities,” Buck said for TopBuild. “Together, we’ll enhance customer service, unlock meaningful cross-selling opportunities, and drive continued growth and operating efficiency. I’m proud of our team’s track record, including a 10-year sales CAGR of 13% and adjusted EPS CAGR of 31%. Thank you to the entire TopBuild team for delivering these exceptional results.”

MDM Analysis: A Clear M&A-Driven Playbook

Any of QXO’s three deals so far would be considered a landmark transaction in building materials distribution, and QXO’s aggressive pace and scaling is historically unheard of in practically any durable goods sector — even though the company has repeatedly stated an ambitious goal of becoming a $50 billion by the middle of the 2030s.

It also validates comments made earlier this year by QXO leadership that the company was pursuing a pipeline of both mid-sized and “transformational” deals.

This one clearly falls into the latter category.

The scale of the transaction places it among the largest ever in building materials distribution — second only to Home Depot’s $18.25 billion acquisition of SRS Distribution in 2024 — and signals continued acceleration in market consolidation amongst its biggest players.

For QXO, the strategy is explicit: use scale, cross-selling opportunities and operational leverage to build toward its long-term target of $50 billion in revenue and $7.5 billion in EBITDA.

With TopBuild, that path just got significantly shorter — and far more visible.

Related Posts

-

BBB is set to buy Lumber Liquidators parent F9 brands for $150 million, following news…

-

The new leader is a veteran of the construction and building supply distribution sector.

-

Kodiak Building Partners to join legacy Beacon as the next major building materials distributor to…