New research shows that North American manufacturers sharply slowed ordering in November — a response to weak demand and mounting uncertainty ahead of a major Supreme Court tariff ruling. Survey data from GEP and S&P Market Intelligence shows deepening supply-chain slack, creating a buyer’s market even as procurement teams wait for clarity on costs and sourcing risk into 2026.

Manufacturers Hit Pause Amid Tariff Uncertainty

North American manufacturers sharply slowed ordering activity in November as they await a potentially consequential Supreme Court ruling on U.S. tariff authority. New data from GEP’s Global Supply Chain Volatility Index shows the region posting one of its steepest drops in supplier demand this year — a signal that industrial buyers are delaying commitments until they gain clarity on whether current tariffs will be upheld, altered or overturned.

MDM’s 3Q25 MarketPulse Report (Premium access)

“Companies are watching the U.S. Supreme Court closely, and most expect a pause or rollback in tariffs,” GEP Vice President of Consulting John Piatek in the firm’s latest research release. “With supply chains this slack, it remains a buyers’ market heading into 2026, and companies have real leverage to secure favorable terms for the year ahead.”

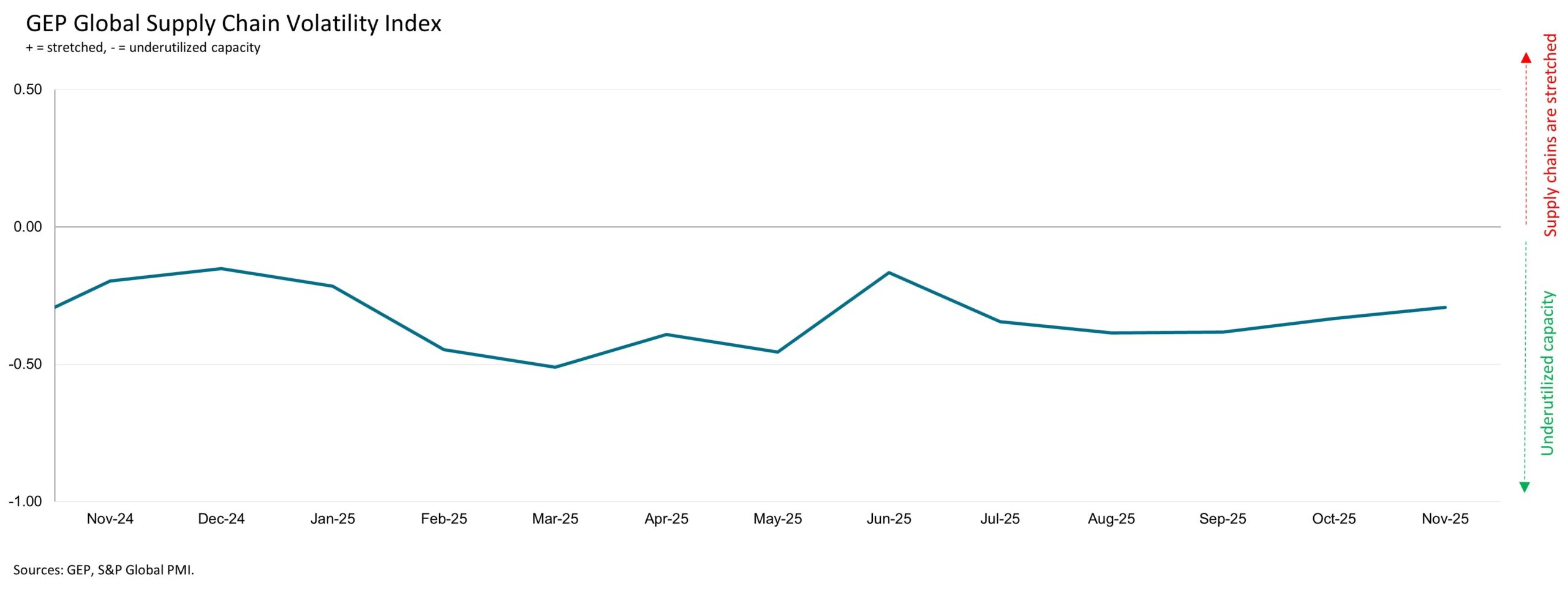

The GEP Global Supply Chain Volatility Index is produced by S&P Global and GEP. It is derived from S&P Global’s PMI surveys, sent to companies in over 40 countries, totaling around 27,000 companies. A value above 0 indicates that supply chain capacity is being stretched and supply chain volatility is increasing, while a value below 0 indicates that supply chain capacity is being underutilized, reducing supply chain volatility.

Global Slack Persists but North America Stands Out

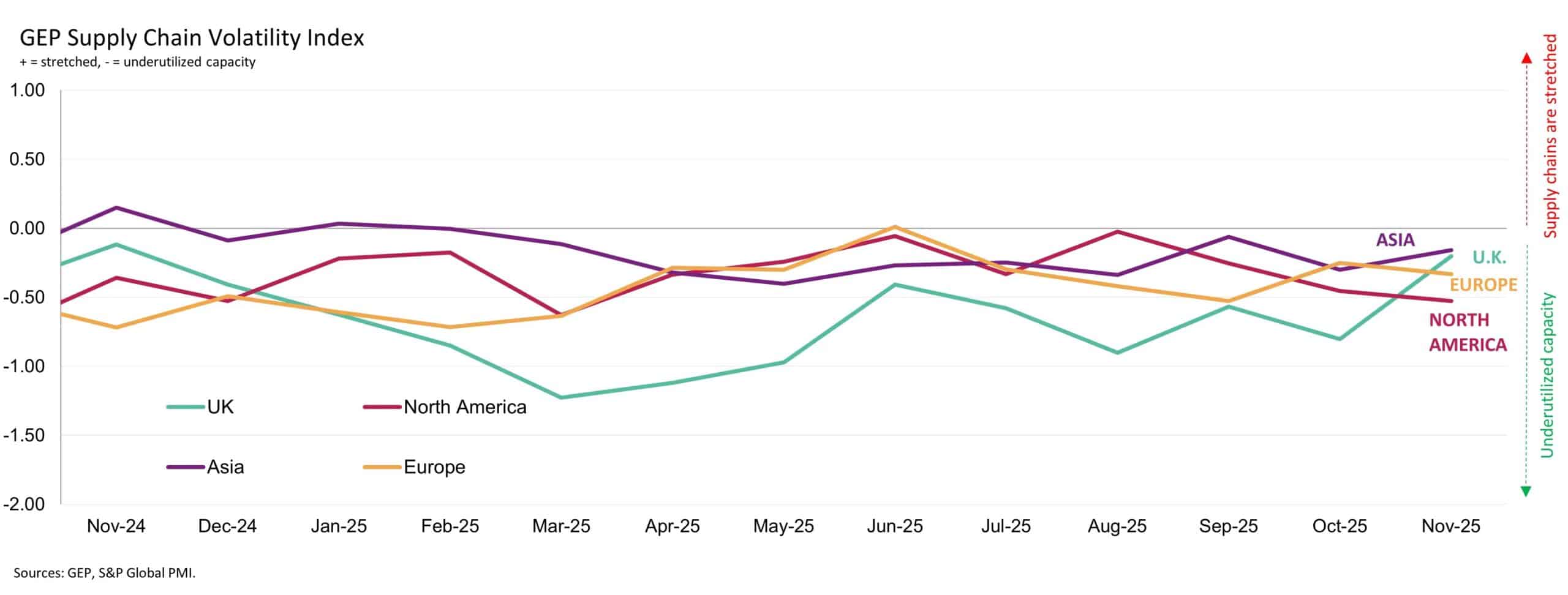

While global supply chains continue to operate with significant spare capacity, the pullback in North America stands out. GEP’s regional index fell to -0.53 in November from -0.45 in October, marking the lowest reading since March and reinforcing what procurement executives across manufacturing sectors have described as a growing caution around new orders. Many are holding off on replenishment, especially for tariff-exposed inputs, despite stable logistics conditions and favorable pricing.

The broader global index, at –0.29, paints a picture of continued slack. Factories worldwide reduced purchases of raw materials and components as demand indicators softened across major industrial regions. Yet the dynamics vary meaningfully by geography. Asia posted a modest improvement as its index rose to -0.16, suggesting slightly tighter utilization driven by resilience in parts of Southeast Asia even as China’s industrial economy continues to work through structural softness. Europe’s reading slipped to -0.33, signaling deeper spare capacity, while the U.K. showed signs of tentative stabilization at –0.20 — its strongest level in about a year, albeit still in negative territory.

A Buyer’s Market Takes Shape

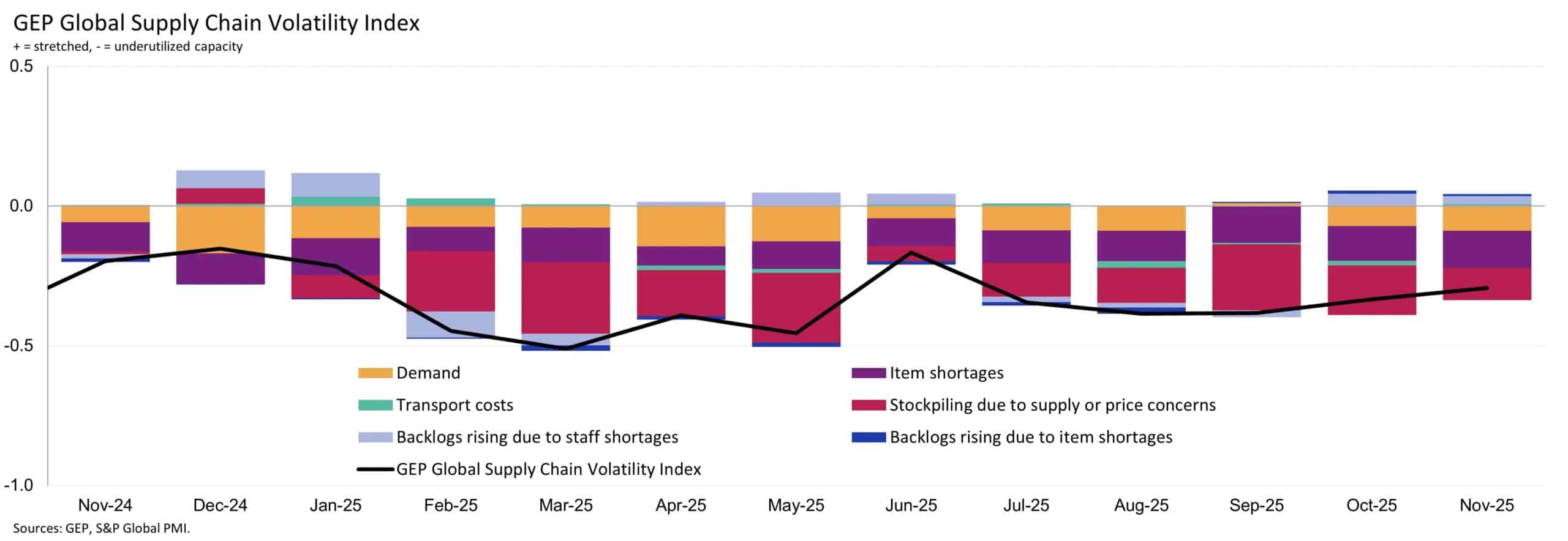

GEP’s underlying indicators reinforce that supply constraints are not the culprit behind today’s slower activity. Material shortages remain well below long-run norms, labor availability is generally adequate and transportation costs sit close to historical averages. Together, these factors have created what GEP calls a “buyer’s market” heading into 2026 — one where suppliers are under mounting pressure to secure volume, and pricing leverage sits firmly with purchasing organizations willing to transact.

Tariff Overhang Drives Strategic Caution

But for many North American manufacturers, the tariff overhang complicates that buyer advantage. The Supreme Court is expected to rule on whether the International Emergency Economic Powers Act legally supports the tariffs imposed in recent years. The decision could reset landed costs almost overnight — with implications that extend from budgeting to supplier diversification strategies — prompting many companies to pause discretionary ordering until the legal landscape is clearer. As a result, stockpiling activity remains historically low, and safety-stock levels show little evidence of defensive rebuilding.

Implications for Distributors and the Road Ahead

For distributors and suppliers that serve industrial end markets, this combination of weak near-term demand and abundant capacity may stretch well into early 2026. Some procurement teams are using the slack period to renegotiate terms, explore alternative sourcing regions or strengthen supplier-risk monitoring as smaller vendors contend with prolonged under-utilization. Others are rethinking inventory policies that had swollen during 2021–2022 but now appear ill-suited for an environment characterized by soft demand and stable supply.

The months ahead will hinge on two variables — the Court’s tariff ruling and the pace of any demand normalization. A favorable ruling for buyers could spur a release of pent-up orders. Conversely, if demand continues to soften or suppliers begin consolidating, the period of excess capacity could evolve into a different kind of supply-chain risk. For now, the data points to continued caution across manufacturing, and a supply-base increasingly shaped by buyers’ needs rather than supply-side constraints.

Related Posts

-

NATS' 19 distributor members and over 60 suppliers will join HDA’s group of over 50…

-

North American robot orders rose in the first half of 2025 as demand grew across…

-

Rexel reported an increase in 2Q sales, driven by strong performance in North America that…